Table of Contents

This year’s Influencer Marketing Benchmark Report is brought to you in collaboration with our partners at Refersion. The report takes an in-depth look at the influencer marketing industry and summarizes the thoughts of more than 2000 marketing agencies, brands, and other relevant professionals regarding the current state of influencer marketing. In addition to the results from our survey, we packed the report with all the influencer marketing benchmarks, metrics and data that matter most to you, along with some predictions of how industry professionals expect it to move over the next year and into the future. Think of it as fuel for your next influencer marketing campaign.

The State of Influencer Marketing Benchmark Report 2022:

Notable Highlights

Influencer Marketing

- Influencer Marketing Industry is set to grow to approximately $16.4 Billion in 2022

- Influencer Marketing focused platforms raised more than $800M in funding in 2021 alone, an indication of the significant growth of the industry

- The global number of Influencer Marketing related service offerings grew by 26% in 2021 alone, to reach a staggering 18,900 firms offering or specializing in Influencer Marketing services

- Instagram influencer fraud has declined over the last few years, still 49% of Instagram Influencer accounts were impacted by fraud in 2021

- More than 75% of brand marketers intend to dedicate a budget to influencer marketing in 2022

- Growth of the Influencer Marketing Industry strongly impacted by an estimated 9% YoY increase in usage of ad blocking tools, with the average global desktop ad blocking rate sitting above 43%

- 54% of the firms working with influencers operate eCommerce stores

- 2021 saw a notable increase in brands paying money to influencers. There is now an equal split between monetary payment and influencers receiving free products

- Zara, the most mentioned brand on Instagram, has an estimated reach of 2,074,000,000

- Netflix Was the Most Followed Brand on TikTok in 2021

- 68% of our marketers plan to increase their influencer marketing spend in 2022

- Instagram was used by nearly 80% of the brands that engage in influencer marketing

Social Commerce

- The value of social commerce sales in 2022 is estimated to be $958 billion

- In just one day in October 2021, two of China’s top live-streamers, Li Jiaqi and Viya, sold $3 billion worth of goods. That’s roughly three times Amazon’s average daily sales

- By 2025, social commerce is expected to account for 17% of all ecommerce spending

Creator Economy

- Creator Economy Market Size is estimated to reach $104 Billion in 2022

- More than 50 million people globally consider themselves content creators

Survey Methodology

We surveyed just over 2000 people from a range of backgrounds. 39% of our respondents considered themselves brands (or brand representatives). 31% work at marketing agencies (including those specializing in influencer marketing), and 3% are PR agencies. We merge the remaining 27% as Other, representing a wide range of occupations and sectors.

We have seen a comparative increase in B2B businesses over B2C firms compared to last year. 62% of those surveyed identify as part of the B2C sector (down from 70% in 2021), with the remaining 38% running B2B campaigns (up from 30%).

The most popular vertical represented remains Fashion & Beauty (15% of respondents), although this is down considerably from last year’s 25%). Health & Fitness remains second with 13%. Travel & Lifestyle respondents rebounded to 12%, closely followed by Gaming at 11%. Family, Parenting & Home (6%) and Sports (4%) remain the other sectors separately shown. The remaining 39%, grouped as Other, covers every other vertical imaginable. This is a 10% increase from last year’s survey, indicating that influencer marketing is no longer just relevant to a few tight niches. Despite this year’s survey sample size being smaller than last year’s, it is still a comprehensive study. Therefore, the proportions of each industry vertical represented here will likely still be typical of influencer marketing users in general.

57% of our respondents came from the USA, 13% Asia (APAC), 11% Europe, 5% Africa, 2% South America, and 11% described their location as Other.

The bulk of our respondents came from relatively small organizations, with 44% representing companies with fewer than ten employees. 26% had 10-50 employees, 11% 50-100, 12% 100-1,000, and 8% coming from large enterprises with more than 1,000 employees. Overall, however, there are slightly fewer respondents from larger organizations than last year, which might have had a small impact on the comparative results.

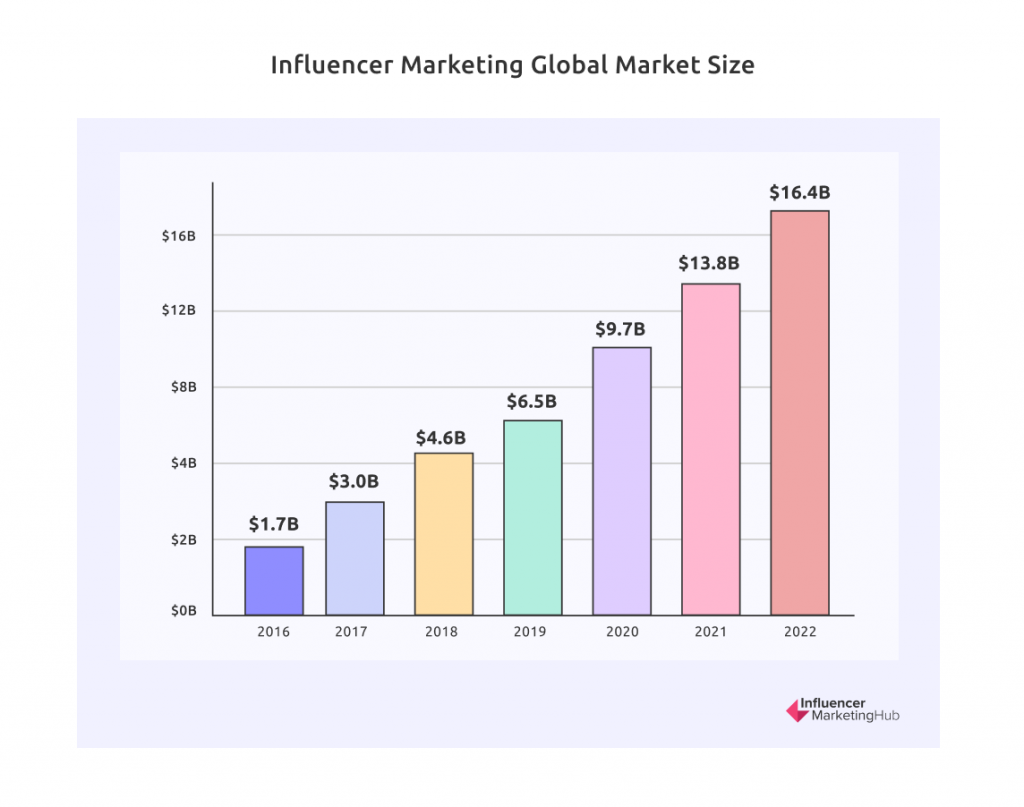

Influencer Marketing Expected to Grow to be Worth $16.4 Billion in 2022

Despite initial concerns that influencer marketing (indeed, all marketing) might decrease due to Covid19, it increased over both 2020 and 2021. Sure, some industries, such as tourism and airlines, initially had to retrench dramatically, but many others adjusted their models to survive in the Covid (and post-COVID) world. And there is even some renewed life in the more Covid-affected industries.

People initially spend considerably more time online than pre-Covid, which hasn’t completely reversed despite many people returning to work. As a result, businesses had to upgrade their websites to cope with increased demand. Looking back through past versions of this Benchmark Report, you will consistently see that actual and estimated influencer marketing has grown dramatically over recent years. Coronavirus accelerated that growth in 2020 and 2021, which is estimated to continue into 2022.

From a mere $1.7 billion at the time of this site’s beginning in 2016, influencer marketing is estimated to have grown to have a market size of $13.8 billion in 2021. Furthermore, this is expected to jump a further 19% to $16.4 billion in 2022.

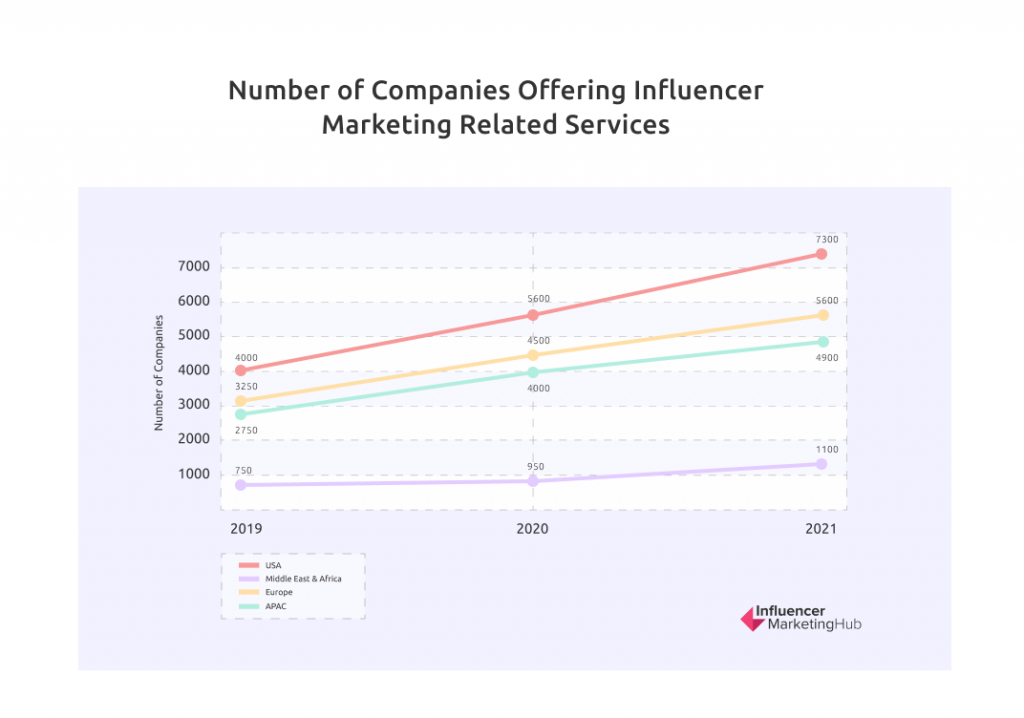

Influencer Marketing Related Services / Companies Continue to Grow

As influencer marketing has matured as an industry, it has attracted support companies and apps to simplify the process for brands and influencers. However, organic influencer marketing can be slow and tedious, particularly when finding and wooing influencers to promote your company’s products or services.

We have only looked at influencer platforms and agencies in the past. But in our Influencer Marketing Benchmark Report 2022, we are widening this to encompass all influencer marketing-related services/companies, including influencer services, agencies, and platforms. We have noticed in our reviews that many of the tools we group as “platforms” offer an ever-increasing variety of services to their customers. These include influencer discovery, influencer marketplaces, eCommerce tools, and product/gifting tools. The days of doing everything organically seem well gone. We have now written 50 reviews at the Influencer Marketing Hub by the beginning of 2022 but have only just scraped the surface of the industry.

Influencer Marketing related services/companies grew 26% in 2021, to 18,900 worldwide. Growth was highest in the United States, which saw a 30% increase in influencer agencies, platforms, and services.

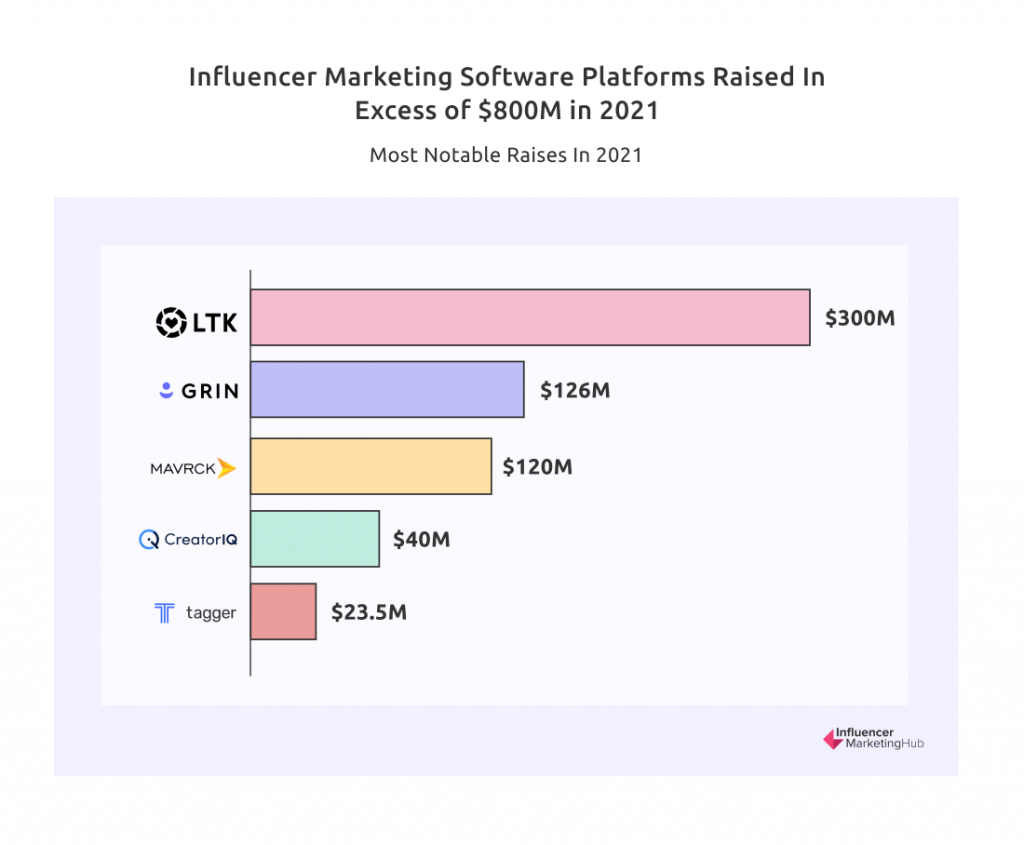

Software Platforms Specifically Focused on the Influencer Marketing Industry Raised More Than $800M in 2021

Many influencer marketing companies can look back fondly on 2021. Investors recognized the success of influencer marketing and the demand for quality tools and invested heavily in some of the newer influencer software platforms. In total, software platforms specifically focused on Influencer Marketing raised more than $800M in 2021.

Some of the platforms to receive investor cash and confidence were:

- Grin – $126M

- Mavrck – $120M

- CreatorIQ – $40M

- Tagger Media – $23.5M

- LTK – $300M

Grin’s funding included $110M in a round led by Lone Pine Capital of Greenwich, Connecticut, that will allow the company to access markets in the United Kingdom and Australia. This followed from $16 million Series A funding earlier in the year led by Imaginary Ventures.

LTK raised $300 million at a $2 billion valuation from SoftBank Vision Fund 2 to scale and build up more global operations.

Social Media User Demographics Statistics

This section highlights some statistics that emphasize the types of people most likely to use social media. When you are searching for influencers to promote your brands, you will want to focus on those influencers who are followed by the type of people most likely to be interested in your products or services. The social media network where each influencer has gained the most fame impacts this – clearly, you want to work with popular people on the same social networks where your potential customers spend their time. Remember, just because you spend time on a particular social network doesn’t mean that your customers do too, particularly if they are of a different demographic to yourself.

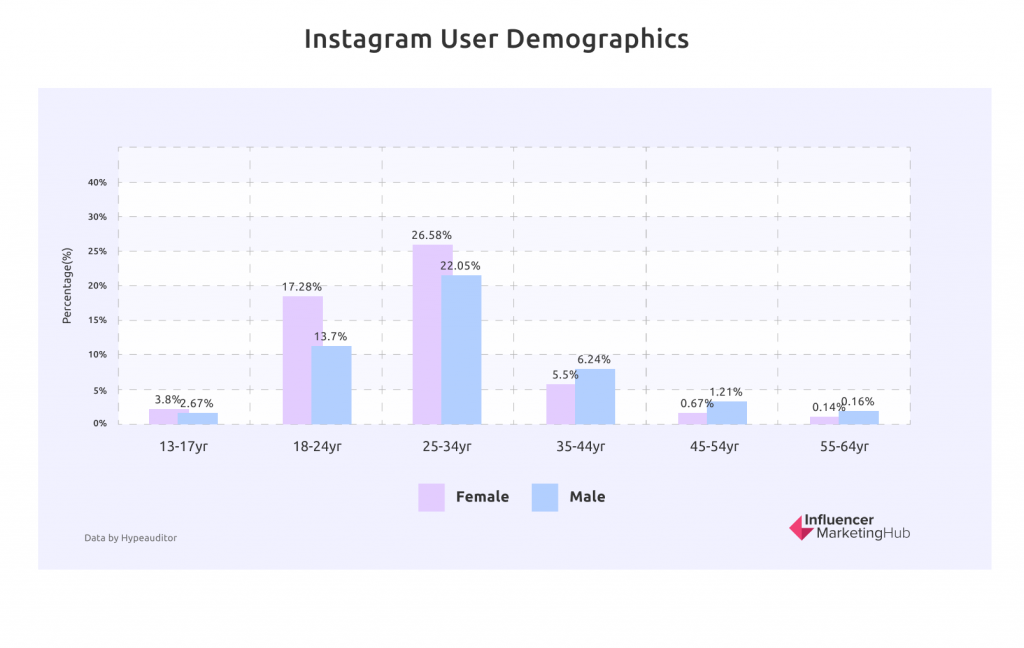

As you can see from the above data, the greatest lovers of Instagram are people aged 25-34, followed by 18–24-year-olds. In both cases, more females than males use Instagram.

One statistical oddity (although numbers are small) is that for age groups 35 and older, the usage of the genders reverse, with more older males using Instagram than their female counterparts.

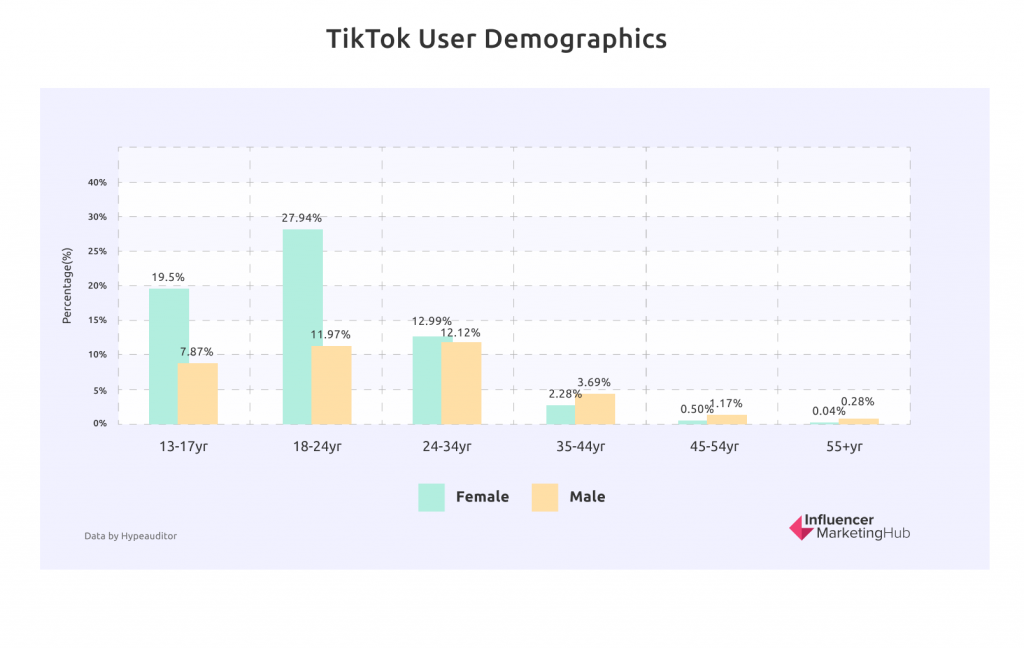

TikTok is the Epicenter of Generation Z

Anybody who knows the younger generations will understand this statistic. TikTok has taken Generation Z with a storm. So, if you wish to market to Gen Z (females at least), you should be searching for TikTok influencers with whom to partner. On the other hand, if you sell to Baby Boomers of Generation X, you can comfortably give TikTok a miss.

The gender split is interesting. There is a distinct female bias amongst TikTok users 24 and younger. Yet things are much more balanced for Millennial TikTok users and substantially male-dominant amongst the few older TikTok users.

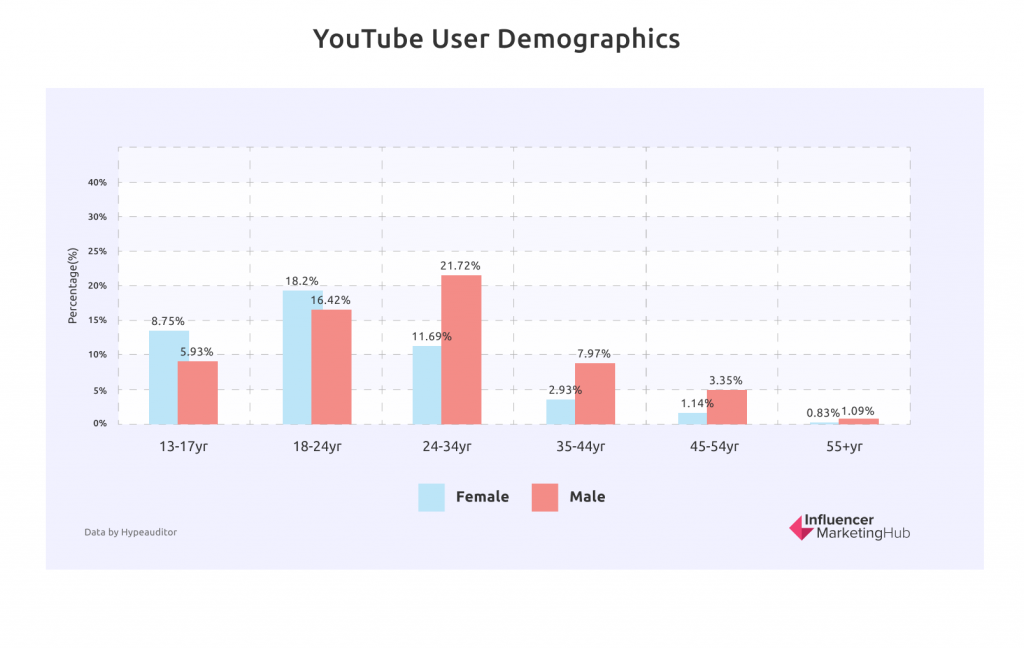

Male YouTuber Viewers Outnumber Females for Millennials and Older Age Groups

In some ways, YouTube is more passive than either Instagram or TikTok. You often tune into YouTube videos in much the same way as you do traditional TV. Although some people love making comments on videos they love (or hate), there is less of a social element for many.

This trend is particularly evident for Millennials (the age group most beloved of Instagram). Male Millennials make up almost a fifth of all YouTube viewers, more than double their female counterparts.

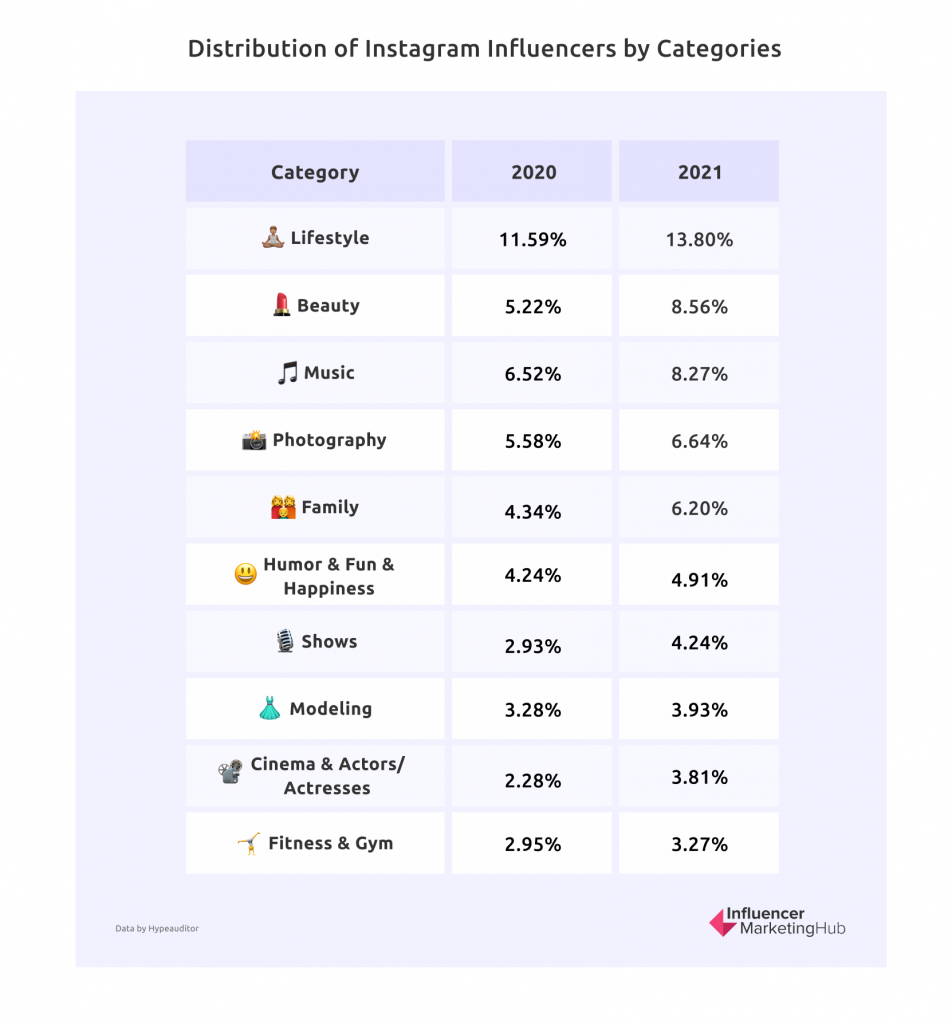

Lifestyle and Beauty Top Instagram Influencer Niches

The most common niche in which Instagram influencers posted in both 2020 and 2021 was Lifestyle. This is no great surprise when you consider which influencers are the best known to most people. In addition, lifestyle is an easy niche to share captivating, vivid images.

Second-placed Beauty is also highly visual, making it an ideal subject for posting on Instagram. Also, when you consider Instagram’s core audience of 25-34 females, it is hardly surprising that beauty influencers would be popular on the platform.

Influencer Engagement

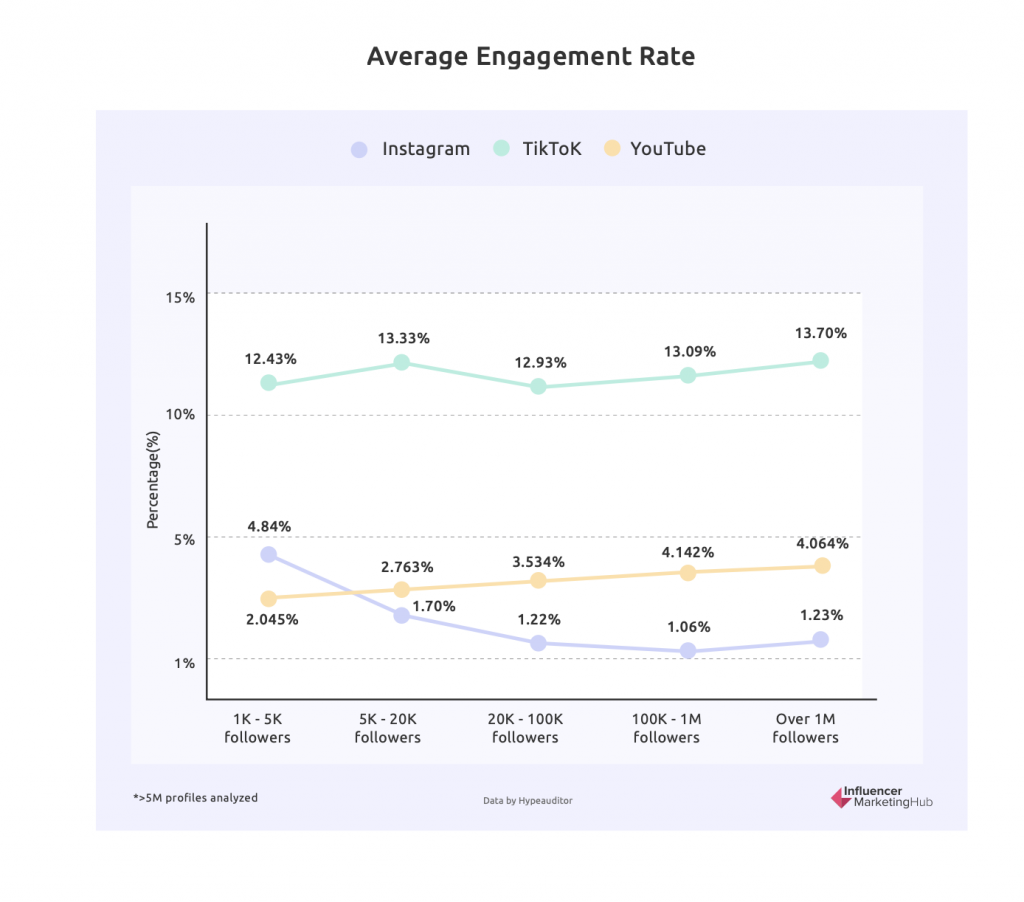

Instagram Influencer Engagement Fell in 2021, But Higher Than in 2019

In all the time we have reported on influencer marketing, we have observed the general pattern of Instagram accounts with large numbers of followers having a lower engagement rate than accounts with fewer followers. This is logical – it is much harder for popular influencers to reply to every comment and engage as closely with each follower as for smaller Instagrammers. This is because people only have limited time to engage. Also, many people deliberately choose to follow popular influencers passively, happily “lurking,” viewing shared images without active participation.

We have seen a general reduction in engagement over the last few years, particularly for medium to large accounts. There was an increase in engagement near the start of Covid in 2020, with more people having time on their hands than the previous year. However, this recovery turned out to be short-lived, with a reduction again in 2021. Yet, engagement is still better than in 2019 for most nano and micro-influencers.

TikTok Engagement High Compared to Other Social Networks, Particularly for Large Influencers

Although most social networks have seen a gradual falling off of engagement for organic posts over recent years (apart from a Covid blip in 2020), TikTok has only seen a relatively small drop. And most importantly, the engagement rate for TikTok influencers is high at all size tiers.

There was one notable change in 2021, however. TikTok now breaks the general rule of social media engagement. Large influencers have the highest engagement rate, while small influencers have the lowest, although that is still high compared to other platforms.

Perhaps this relates to the strength of TikTok’s algorithm in targeting content to match the interests of its viewers. TikTok is likely to be intelligently targeting the videos of its most popular influencers into many users’ For You feeds.

Larger YouTube Channels Have Better Engagement Than Smaller Channels

YouTube also breaks the general rule of social media, with larger YouTube channels having higher engagement rates than smaller channels. Technically, channels with 100K-1M followers have the highest engagement rate, but huge YouTube influencers (1M+ followers) aren’t far behind.

Instagram Influencer Fraud Has Declined Over the Last Few Years

A couple of years ago, influencer fraud was a significant discussion point. Indeed, there was a danger that influencer fraud could stop the still-nascent industry in its tracks.

Since then, many tools and platforms have been developed that detect influencer fraud. As a result, the percentage of influencer accounts impacted by fraud has fallen across the board, now less than 50%.

As the data here indicate, it is still a problem for many influencers. It is advisable for brands to use available tools to ensure influencer authenticity when searching for suitable influencers.

It is important to remember that despite everything being lumped together as ‘influencer fraud”, in many cases, the influencers are the victims, not the perpetrators. For this report, we consider “influencers impacted by fraud” to be Instagram accounts with over 1000 followers with growth anomalies or inauthentic engagement (comments and likes from bots, giveaway comments, comments from Pods, etc.) Not all influencers impacted by fraud do so on purpose. On average, 49.23% of influencers globally are affected by fraud.

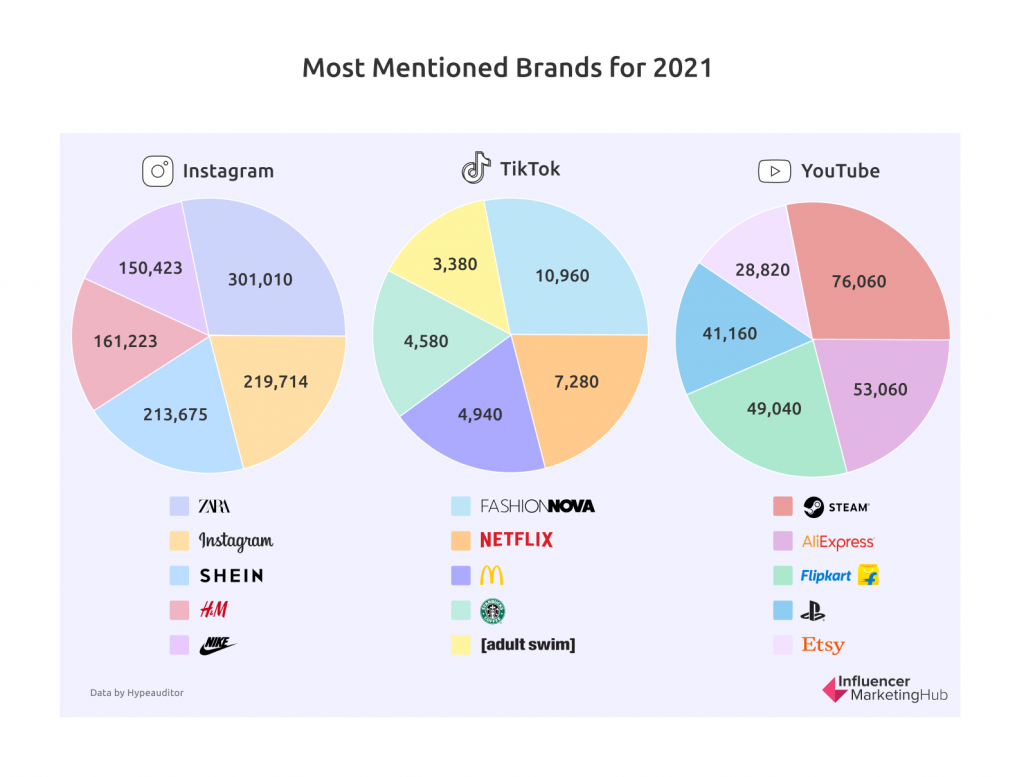

The Most Mentioned Brands on Social Media in 2021

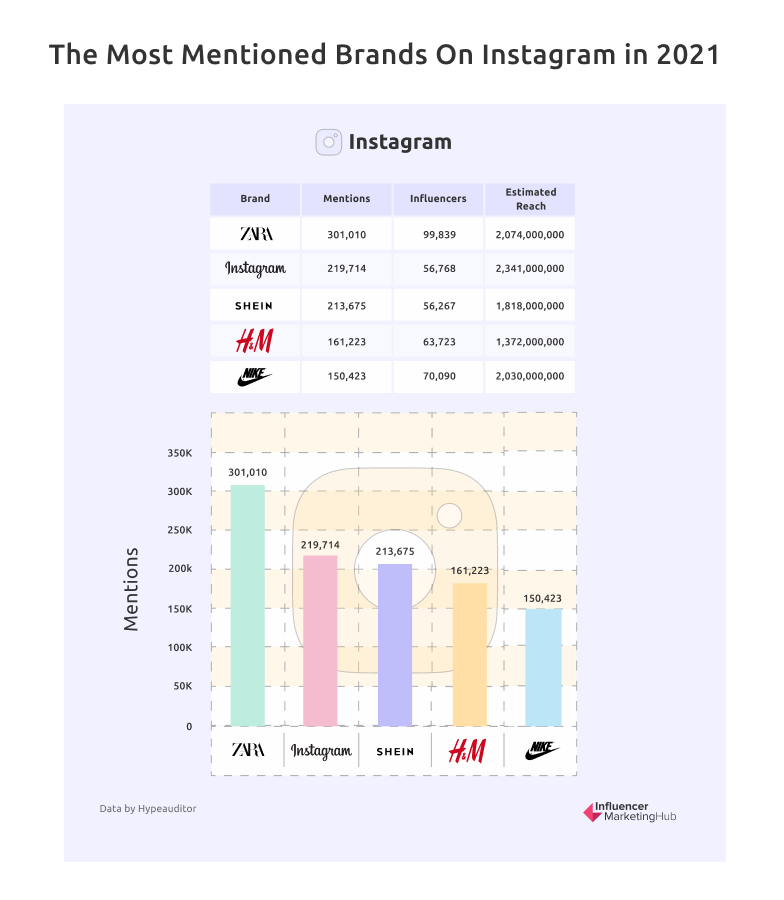

Zara Was the Most Mentioned Brand on Instagram in 2021

Zara will be loving the more than 300K Instagram mentions it received in 2021. Of course, it helped that it had nearly 100K influencers posting and sharing about their products, with a combined reach of more than 2 billion people.

Notably, Zara, Nike, and H&M all received more mentions on Instagram than Instagram itself. And also, YouTube managed to take tenth position … on Instagram.

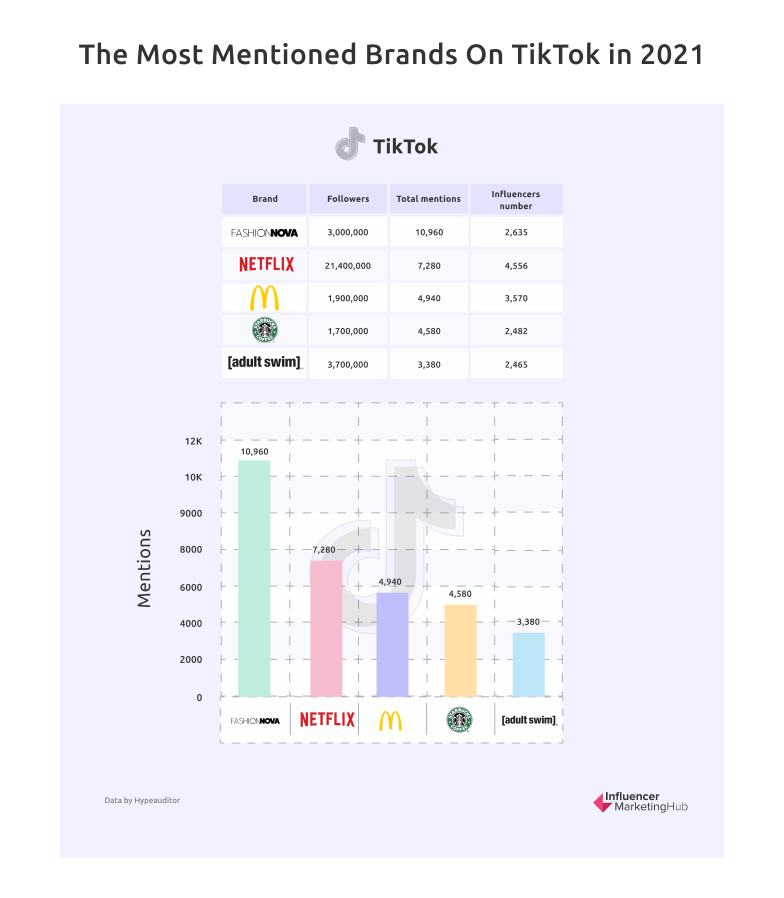

Netflix Was the Most Followed Brand on TikTok in 2021

TikTok also saw an interesting cross-brand trend in 2021. Video streamer, Netflix, was the most followed brand on the short video platform, TikTok. So, if people weren’t watching videos on Netflix, they were talking and making videos about what they’d streamed on TikTok. Disney also made it into the top 10 brands on TikTok, as did CBS News. Who said watching TV was dead and that today’s youth don’t take an interest in the news?

Interestingly, another of the most followed and mentioned channels on TikTok was Barstool Sports. Barstool Sports is a sports and pop culture blog covering each day’s latest news and viral highlights with blogs, videos, and podcasts.

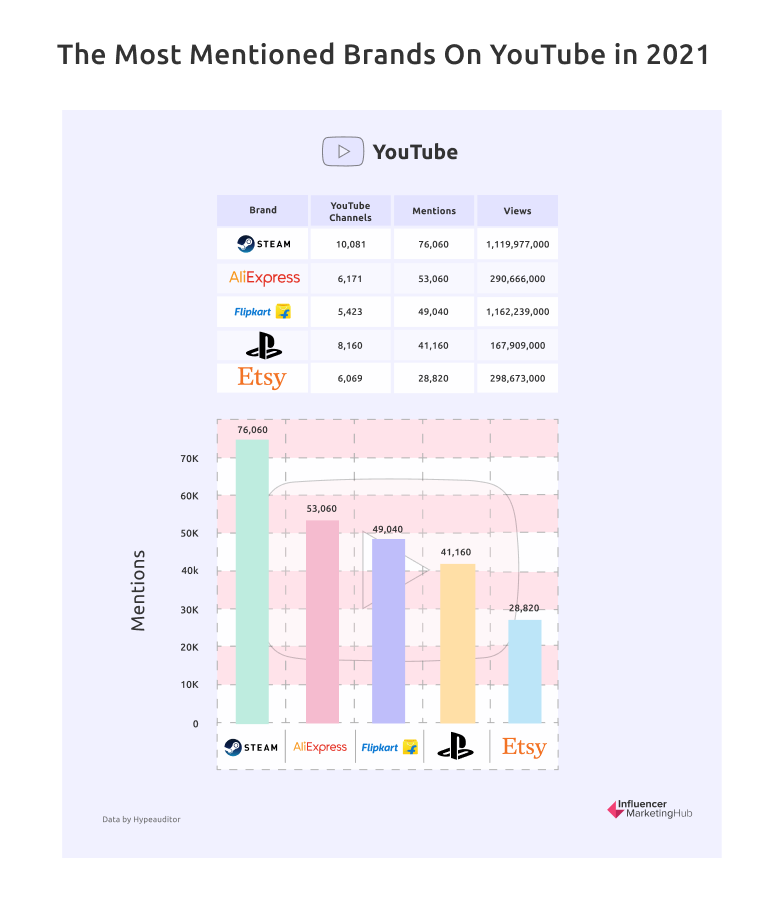

Steam is the Most Followed Brand on YouTube

The YouTube channels with the most mentions and views relate to either gaming (Steam, PlayStation, Microsoft, and Roblox) or shopping (AliExpress, Flipkart, Shein, and Etsy). While most of the 10,000 channels connected to Steam aren’t directly related to the Steam platform, they cover games that you can purchase in the Steam store. Likewise, the channels allocated to PlayStation and Microsoft are most likely channels specific to games on those systems.

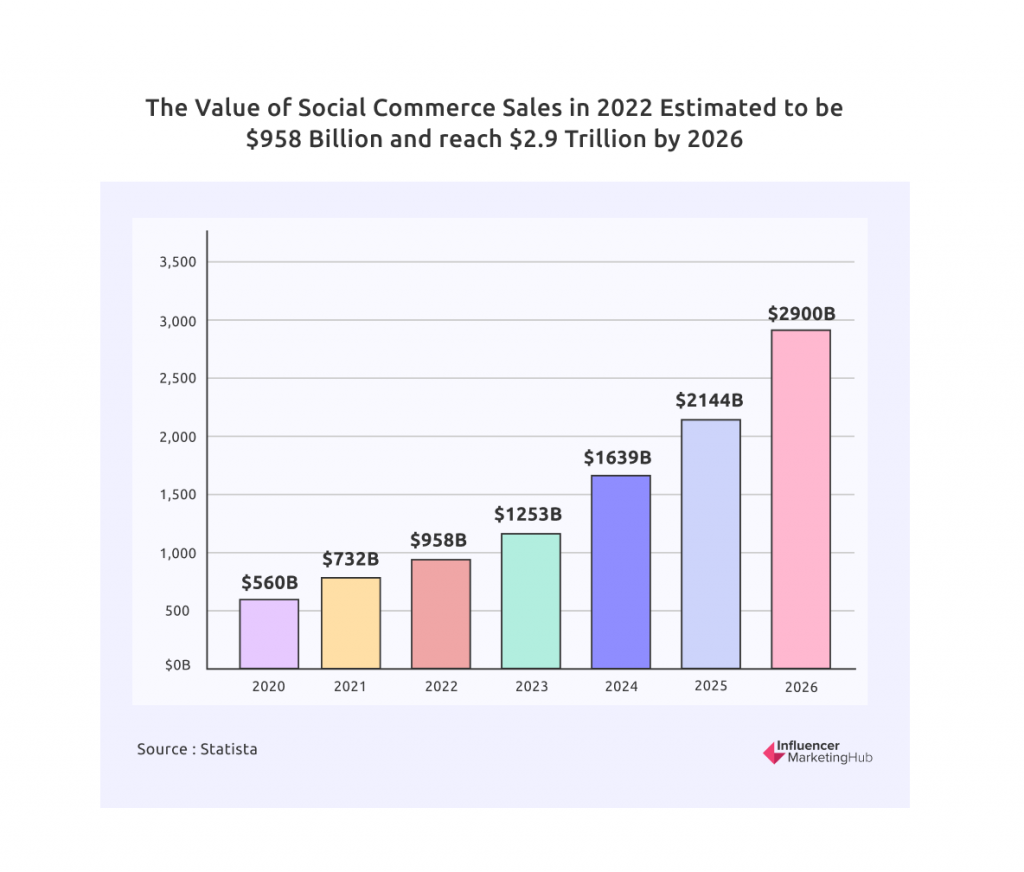

The Value of Social Commerce Sales in 2022 Estimated to be $958 Billion

Global sales through social media platforms were estimated to be $560 billion in 2020. And social commerce sales have continued to rise at increasing rates since then, with many people now preferring to shop from home using their phones. As a result, it is estimated that the value of social commerce sales will reach $958 billion in 2022, potentially reaching $2.9 trillion by 2026.

Estimates currently place the YoY market growth of social commerce at 30.8%. By 2025, social commerce is expected to account for 17% of all eCommerce spending.

Social commerce has particularly taken off in China, where nearly one in two internet users purchased from social networks in 2021. In just one day in October 2021, two Chinese live-streamers, Li Jiaqi and Viya, sold $3 billion worth of goods, equivalent to three times Amazon’s average daily sales.

However, the West has been slower to see the benefits of social commerce. There was an estimated $51.2 billion of social commerce sales in the US in 2021, giving it a 6.9% share in the global market. Expect to see increased social sales there over the next few years, though.

Creator Economy Estimated Market Size $104 Billion

Use a suitable image as shown in the relevant section of the Google doc (headed as above)

The Creator Economy has grown dramatically over the last few years. More than 50 million people globally now consider themselves content creators, and the market size has grown to well over $104 billion. In our most recent Creator Earnings: Benchmark Report, we calculated the total Creator Economy market size to be around $104.2 billion and on par with a substantial growth trajectory similar to the Gig Economy.

Investors contributed an estimated $1.3 billion+ of venture capital in the Creator Economy in 2021, indicating a high level of confidence in the sector.

Kajabi, the online course platform, was the top-funded company on our market map, having drawn $550 million in investment at a $2 billion valuation. Other notable VC investments into the Creator Economy last year included:

- Cameo (the personalized video shout-out app) who garnered more than $166 million in total funding for a $1 billion valuation,

- Substack (the newsletter platform), who raised a total of $82 million at a valuation of $650 million,

- VSCO (the photo-editing app), now valued at $550 million, after raising $85 million in funding, and

- Splice (the audio-editing platform), now valued at $500M, with backers like Union Square Ventures, True Ventures, First Round Capital, and Lerer Hippeau Ventures.

The FTC Sent Hundreds of Businesses Warnings About Fake Reviews and Other Misleading Endorsements

Use a suitable image as shown in the relevant section of the Google doc (headed as above)

The FTC continued to scrutinize the online activities of businesses, sending out over 700 Notice of Penalty Offenses letters in October 2021 alone to large companies, top advertisers, leading retailers, well-known consumer product companies, and major advertising agencies. These included high-profile businesses including Adobe, Amazon, Apple, AT&T, Barnes & Noble, Facebook, Ford Motor Co, General Electric, Google, McDonald’s, and Microsoft. By sending a Notice of Penalty Offenses, the agency placed the companies on notice they could incur significant civil penalties—up to $43,792 per violation—if they use endorsements in ways that run counter to prior FTC administrative cases.

In the UK, complaints to the ASA on this subject also remain high. The ASA released Influencer Ad Disclosure on Social Media, a report into Influencers’ rate of compliance of ad disclosure on Instagram in March 2021. They analyzed 24,000 individual ‘Stories,’ posts, IGTV, and reels across 122 UK-based influencers. They found a disappointing overall compliance rate with the rules on making it sufficiently clear when they were being paid to promote a product or service. 2020 saw a 55% increase on 2019 in complaints received about influencers, from 1,979 to 3,144 individual complaints. 61% of those complaints in 2020 were about ad disclosure on Instagram. The ASA has yet to indicate whether things improved in 2021.

Most of the following points come from this year’s Benchmark survey. You could choose to reuse some of the more general images on the site, although you will need to update graphs and tables for this year’s figures.

Sizeable Increase in Content in Recent Years

We asked our respondents whether they had increased content output over the last two years. A massive 84% of them admitted to having upped the amount of content they produced. This is up on last year’s 80% and remember that these figures are cumulative. 84% of the respondents of the 2019 survey had also said they had increased content.

Clearly, many firms now realize the insatiable demand for online content and have increased their content marketing accordingly, year after year. Judging by the increased uptake in influencer marketing over the last few years, much of this increase in content must be created and delivered by influencers on behalf of brands. Clearly, new content is continually being developed, some of it being shared over comparatively new social networks like TikTok.

An Increasing Majority Have a Standalone Budget for Content Marketing

The majority (61%) admit to having a standalone budget for content marketing. This figure is creeping up each year and is up from 59% last year and 55% in our 2020 survey.

Yet, although these figures are over 50%, they are surprisingly low. For example, HubSpot reports that 82% of their respondents used content marketing in 2021, up from 70% in 2020.

Perhaps the discrepancy simply reflects that some firms operate a single marketing budget rather than separating it into the different types of marketing they use.

The Vast Majority of Respondents Believe Influencer Marketing to be Effective

Unsurprisingly, considering the overall positive sentiment expressed about influencer marketing, just over 90% of our survey respondents believe influencer marketing is an effective form of marketing.

This statistic has hovered around the same level in each of our surveys since 2017. It is clear that most firms that try influencer marketing are happy with the results and are willing to continue with the practice. You may read the odd horror story in the media, but that is the exception to the rule. Most influencer marketing partnerships work and are a win-win situation for all parties.

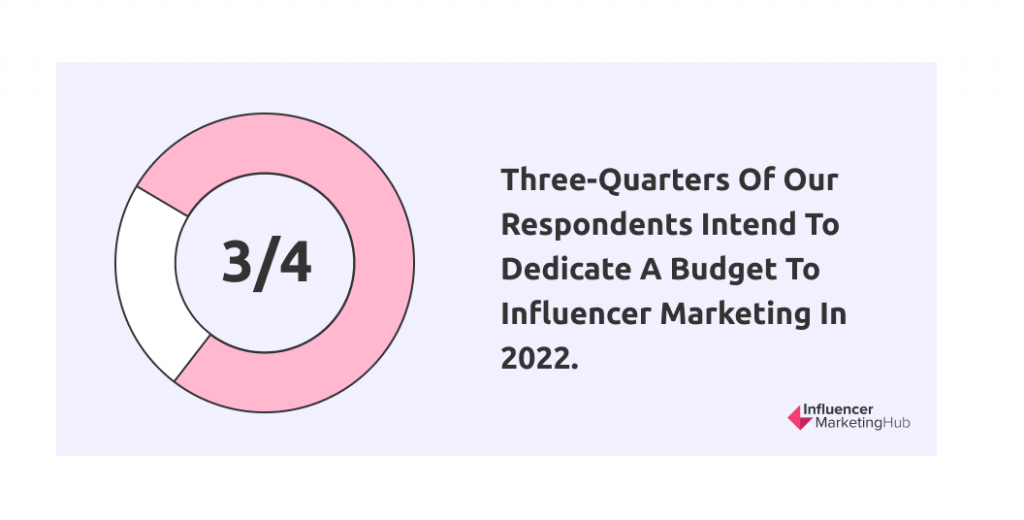

More Than Three-Quarters of Our Respondents Intend to Dedicate a Budget to Influencer Marketing in 2022

The general satisfaction felt by firms that have engaged in influencer marketing seems to flow through to their future planning. For example, 77% of our respondents indicated that they would be dedicating a budget to influencer marketing in 2022.

This is an increase on last year’s 75% result and well up on the 37% who claimed they would dedicate a budget in our first survey in 2017. This slight increase could result from firms increasing marketing back to pre-Covid levels.

68% of Respondents Intend to Increase Their Influencer Marketing Spend in 2022

68% of those respondents who budget for influencer marketing intend to increase their influencer marketing budget over the next 12 months. An additional 14% indicate that they expect to keep their budgets the same as in 2021. A further 16% stated that they were unsure how their influencer marketing budgets would change. This leaves a mere 3% intending to decrease their influencer marketing budgets.

These results suggest significantly increased spending on influencer marketing in 2022, after the uncertainty of 2020 and 2021. This year, the 3% planning to decrease their influencer marketing budget is less than half 2021’s 7% figure.

Overall, this is further proof that influencer marketing remains successful and shows no sign of disappearing or being just a fad. After a few years of robust growth in influencer marketing, you might have anticipated marketing budgets to have shifted to “the next big thing.” However, that hasn’t happened. Brands and marketers recognize the effectiveness of influencer marketing and are not searching for something new.

Two-Thirds of Respondents Intend to Spend Between 10% and 30% of Their Marketing Budget on Influencer Marketing

Influencer marketing is, of course, merely one part of the marketing mix. Most businesses balance their marketing budget across a wide range of media to reach the greatest possible relevant audience. However, as we saw above, 77% of our respondents’ firms intend to include some influencer marketing in their mix.

This year, we noticed that while more firms intend to allocate some marketing spending to influencer spending, fewer firms intend to devote their largest share towards it. Instead, brands appear to be spreading their marketing across a broader range of channels.

5% of respondents are clear fans of influencer marketing, intending to spend more than 40% of their marketing budget on influencer campaigns. However, this is a noticeable decrease on 2021’s 11% and 2020’s 9%.

9% of respondents intend to devote 30-40% of their marketing budget to influencer marketing, marginally down on last year’s statistics. An additional 28% plan to allocate 20-30% of their total marketing spending to influencer marketing. This is considerably greater than last year’s 19% assigning this level of marketing budget.

The most common percentage of marketing devoted to influencer marketing comes in the 10-20% range, with 39% of respondents intending to spend in this range, up slightly on 2021 figures. A mere 19% expect to spend less than 10%.

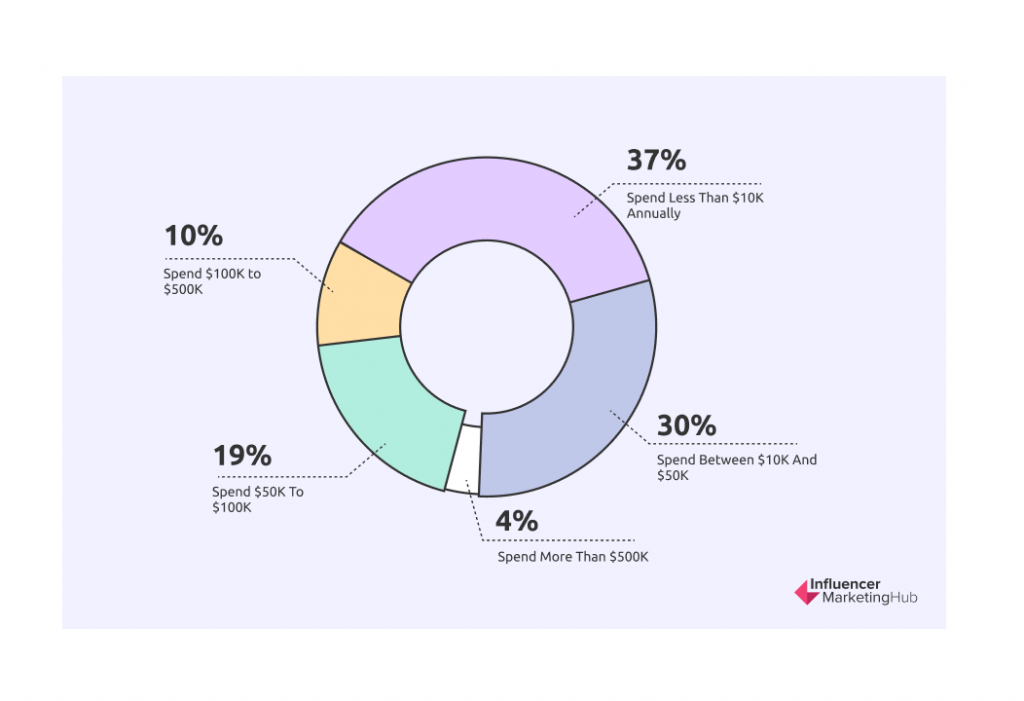

Although Most Brands Spend Less Than $50K on Influencer Marketing, Nearly 4% Spend More than $500K

Brands of all sizes engage in influencer marketing. Therefore, it should be no surprise to see quite some variation on what firms spend on the activity. 37% of the brands surveyed said they spend less than $10K annually on influencer marketing (notably lower than last year’s 49%, perhaps an indication of the world reopening after Covid lockdowns). 30% spend between $10K and $50K. A further 19% spend $50K to $100K (up notably on last year), 10% $100K to $500K (also higher), and 4% spend more than $500K.

Clearly, the amount that a firm spends depends on its total marketing budget and the proportion it chooses to devote to influencer marketing. Those brands that opt to work with mega-influencers and celebrities spend more than brands that work alongside micro- or nano-influencers. After two years of Covid increasing the extremes – firms either decreasing or increasing their influencer marketing noticeably – we have noticed a leveling out of budgeted spending this year.

Firms Value Working with Influencers They Know

We asked our respondents whether they had worked with the same influencers across different campaigns. The majority, 57% said they had, versus 43% who claimed to use other influencers for their campaigns (or perhaps had only had one campaign so far). These figures are little changed from those reported in 2021.

Clearly, brands prefer to build relationships with existing influencers rather than go through the entire influencer selection process every time they run a campaign. Of course, some firms will have a range of influencers they call upon depending on the nature of a particular campaign, the products they are trying to promote, and the target market. The slight increase (1%) in firms working with existing influencers probably just indicates the natural increase in influencer-business relationships over time.

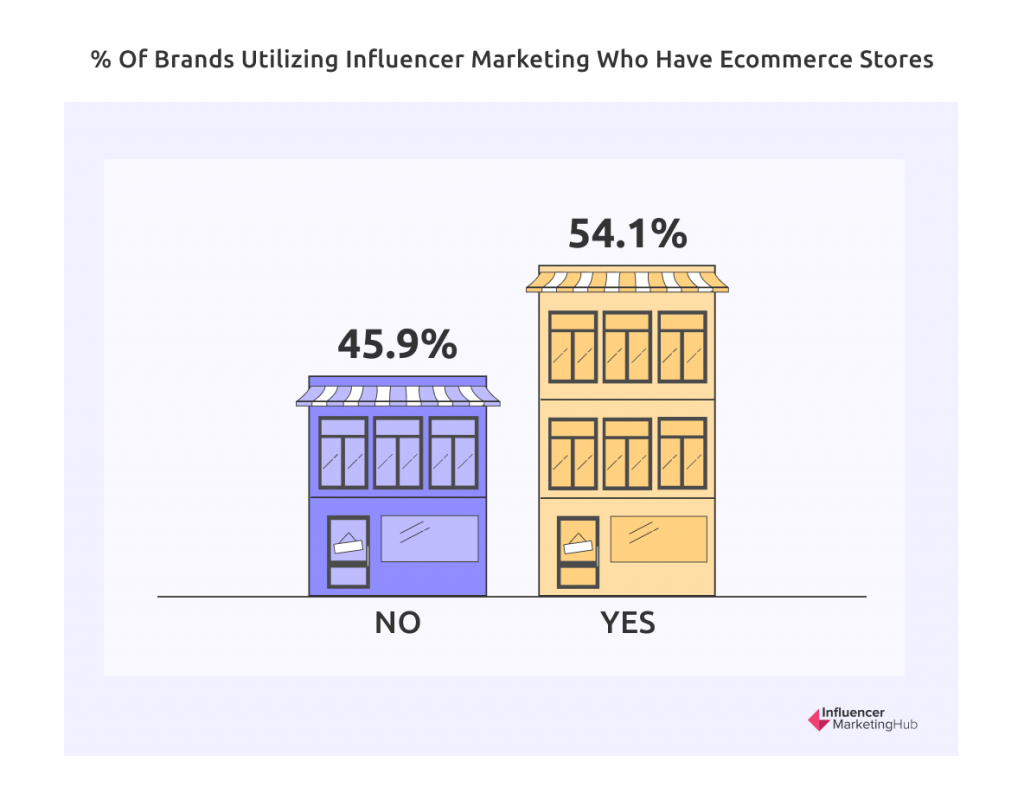

54% of the Firms Working with Influencers Operate eCommerce Stores

Slightly more of our respondents operate eCommerce stores than those who don’t. For example, 54% of the respondents run eCommerce stores versus 45% not doing so. This is a small but noticeable increase in the percentage of influencer-contracting brands operating eCommerce stores. Last year, almost exactly half of such brands ran eCommerce stores.

This is surprisingly high. Remember that our survey respondents come from various backgrounds – brands, marketing agencies, PR agencies, and “Other.” Clearly, eCommerce is increasing in popularity for all types of businesses.

However, one thing to be aware of is that the Influencer Marketing Hub now caters better to eCommerce. A more significant portion of the site is now devoted to articles about that sector. As a result, we may have a higher percentage of eCommerce marketers visiting the site and answering our survey than previously.

More Than One-Third of Respondents’ eCommerce Sites Use Shopify Technology

Shopify is the fastest growing online store builder, being used for 3.2% of all websites (both eCommerce and non-eCommerce) in 2021 (up from just 1.9% in 2020 and a mere 0.1% back in 2014). As a result, it has the highest share of the market for online store solutions. BuiltWith reports that Shopify has a market share of 32% in the United States for websites using eCommerce technologies.

Shopify enjoys an even greater platform market share for the brands with eCommerce stores in our survey, with 36.7% of the stores using Shopify. WooCommerce (which sits on top of WordPress) comes in second place, followed by BigCommerce, Shopify Plus. Salesforce Commerce Cloud, and Magento. A sizable 29.2% of respondents selected Other, suggesting their sites are probably custom-built.

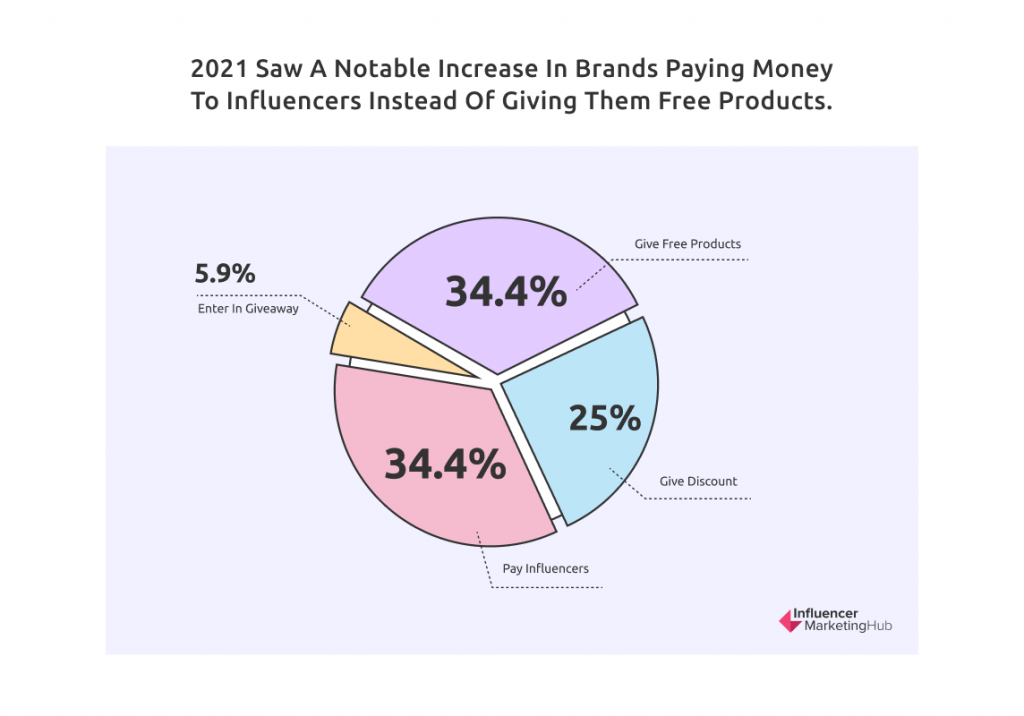

As Many Brands Now Pay Influencers as Give Them Free Product Samples

There was a notable change in the answers to this question this year. Previously, those giving free samples outnumbered those paying cash to influencers. This year, as many respondents (34.4%) admitted to paying money to influencers as giving them free products. In addition, 25% gave their influencers a discount on their product or services (presumably more expensive items), and a much reduced 5.9% entered their influencers in a giveaway.

While more brands are willing to pay influencers for their marketing services, 34.4% is still a relatively low percentage. It probably indicates how many firms work with micro and nano-influencers. These relative newcomers are happy to receive payment in kind rather than cash. Presumably, it is mainly large firms with more sizable marketing budgets that pay influencers with money.

Nearly Half of Payments to Influencers are Made at a Flat Rate

We asked those respondents who paid their influencers a new question this year about how they structured their monetary rewards. The most common method (49%) was paying at a flat rate. However, a sizable percentage of other brands (42%) structured their influencer marketing payments more like affiliate marketing payments by paying a percentage of any sales made as a result of the influencer marketing. Payments based on product level (4%) and tiered incentives (4%) were less common.

PayPal is Still the Most Popular Way to Pay influencers, Although Other Methods Are Common

Isolating those respondents who pay money to influencers, we asked them their preferred payment method. 34% chose PayPal, 24% a third-party payment service (for example, TransferWise), 24% said they paid manually, and 18% paid by wire transfer. This is the first year that we have included manual payments in this question. These include payments made by cash on delivery (COD), money orders, bank transfers, and even email money transfers in some locations like Canada.

In reality, payment methods depend very much on the location of the influencers. If they are based in a different country from where you operate, PayPal or something like TransferWise is much easier than wire transfer or a manual transaction.

More Than 70% of Brands Track Sales from Influencer Campaigns

Although there are many potential goals for an influencer marketing campaign, it is clear that the majority of firms now undertake influencer marketing to drive sales. Indeed 71% of our survey respondents stated that they track sales from their influencer campaigns.

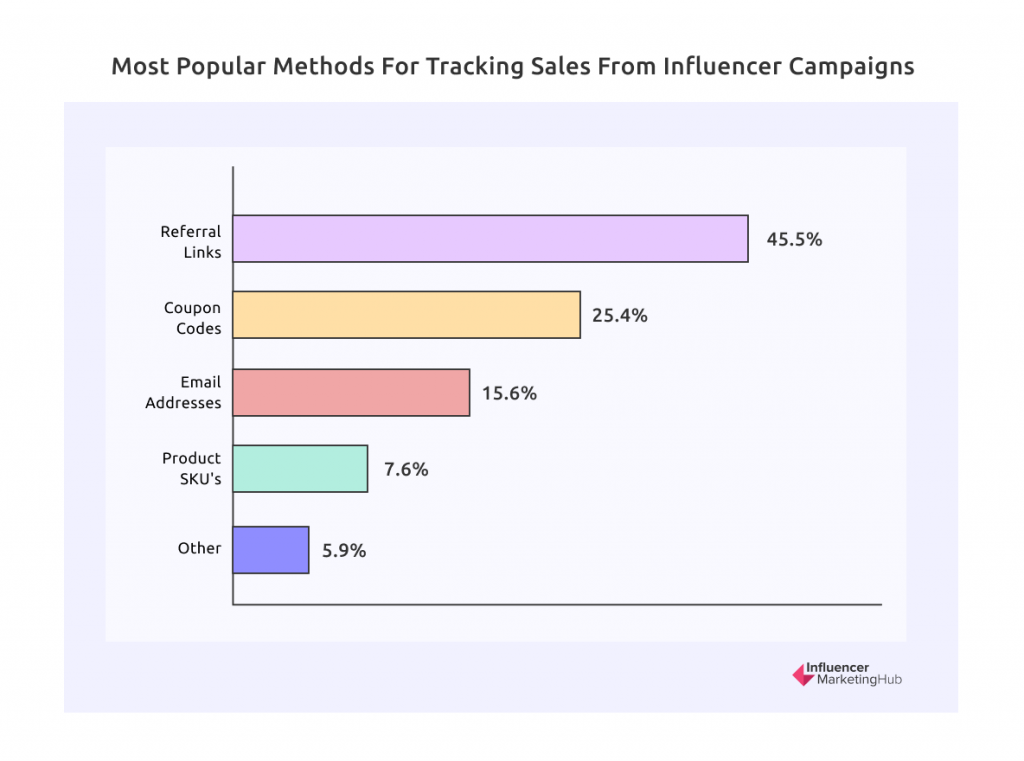

45% of Respondents Track Sales Using Referral Links

Those who tracked sales from their influencer campaigns were asked about their methods of determining these influencer-generated sales. People could select multiple options if they used more than one.

The most common method (45.5%) was to use referral links. Other methods used included coupon codes (25.4%), email addresses (15.6%), and product SKUs (7.6%).

Many Firms Use Influencers for Affiliate Campaigns

This question is somewhat different from what we included in last year’s report, where we simply asked firms whether they used influencers for affiliate campaigns (59% said they did). This year we asked our respondents about the general types of influencer sites they used.

While some people claim blogging is dead, the reality is very different. Nearly 28% of our respondents used bloggers to assist with their affiliate marketing. Other common categories included review sites (19%), coupon sites (15%), newsletters (7%), editorial sites (6.5%), and a sizable group lumped together as “Other” (23%).

2/3 Recognize the High Quality of Customers from Influencer Marketing Campaigns

Brands carry out influencer marketing for a range of purposes. Many campaigns are designed to increase brand awareness rather than encourage sales. This is because some customers are more lucrative for a business than others – they buy high-margin products and add-ons. In some cases, influencer marketing may bring new customers to the brand, but the additional spending may be less than the cost of running the campaign.

Our survey respondents are generally optimistic about the value of influencer marketing overall. Most agree that influencer marketing attracts high-quality customers. In addition, 67% believe that the quality of customers from influencer marketing campaigns is better than other marketing types.

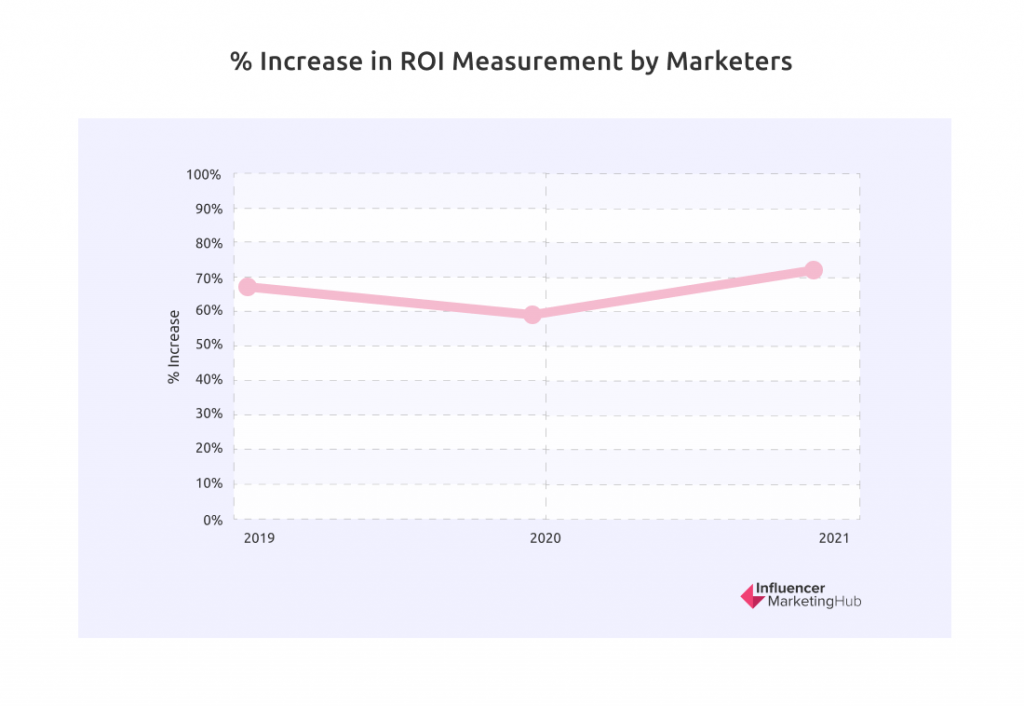

70% Measure the ROI on Their Influencer Marketing

We saw above that 71% of our survey respondents stated that they track sales from their influencer campaigns. Therefore, it should be no surprise that a similar number (70%) also measures the ROI from their influencer campaigns. This improves 2021’s 67% and 2020’s 65% results.

This year’s 70% is the equal highest rate we have seen since the inception of this survey, with the results since 2017 all falling in the range of 65-70%. It is somewhat surprising that 30% of firms don’t measure their ROI. You would think that every firm would want to know how effective their marketing spending is. It would be interesting to know if the bulk of the firms not measuring ROI are those who merely give influencers a product discount rather than paying them directly.

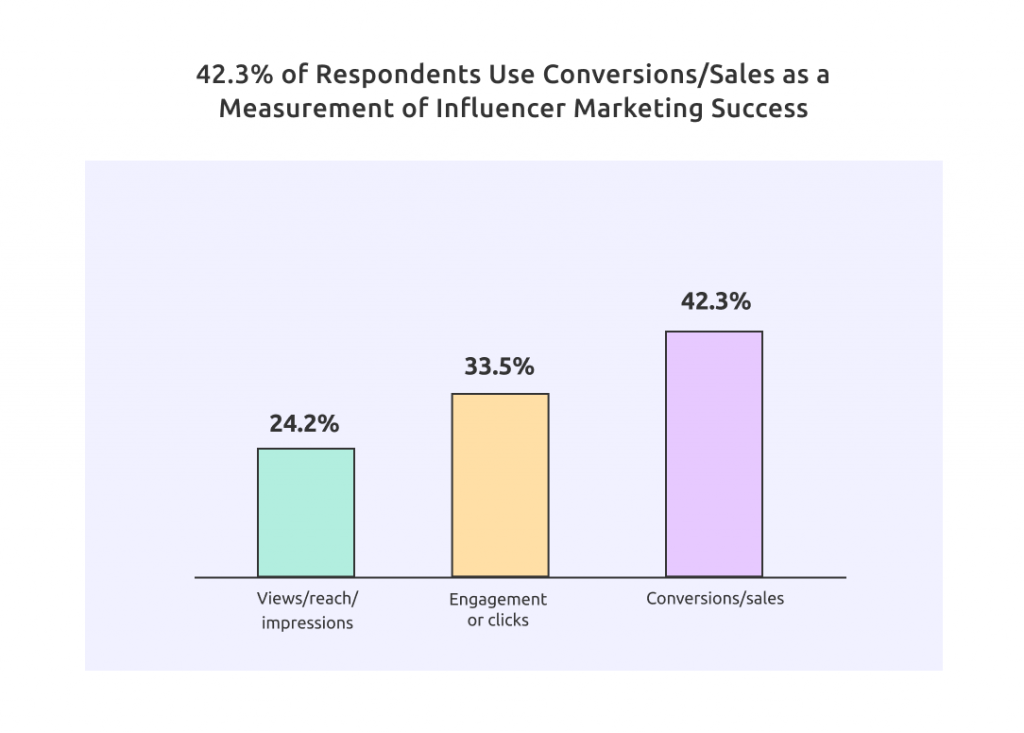

The Most Common Measure of Influencer Marketing Success is Conversions / Sales

This result is also consistent with our earlier results about the percentage of businesses that track sales. In 2019 and preceding years, influencer marketing measurement’s focus was relatively evenly balanced between differing campaign goals, but Conversion/Sales was the least-supported reason. However, in 2020 things changed, with Conversions/Sales taking a clear, undisputed lead, which it has kept ever since.

Influencer marketing is sufficiently widespread now that most businesses understand that the best way to measure your influencer marketing ROI is by using a metric that measures your campaigns’ goals. Clearly, more brands now focus on using their influencer marketing to generate tangible results. 42.3% believe that you should gauge a campaign by the conversions/sales that result.

The remaining respondents have differing goals for their campaign, with 33.5% most interested in engagement or clicks generated due to a campaign (this topped pre-2020 polls), and 24.2% interested in views/reach/impression (down from 29% last year).

Most Consider Earned Media Value a Good Measure of ROI

Earned Media Value has become more recognized in recent years as a good measure of influencer campaigns’ ROI. We asked our respondents whether they considered it a fair representation. This year, 80% favor the measure against 20% who don’t. This result is unchanged from last year.

Earned Media Value provides a proxy for the returns on the posts that an influencer has historically given the firms they have worked with. It indicates what an equivalent advertising campaign would cost for the same effect. EMV calculates the worth you receive from content shared by an influencer.

The only negative of using this measure is that the calculation of EMV can be complicated. As such, it can sometimes be difficult for marketers to explain the concepts to their managers.

Another name used for earned media value when related to influencer marketing is influencer media value, which we have written about in What Exactly is an Influencer’s Media Value.

Presumably, most of the 20% against using the statistic either don’t understand it or struggle to communicate its worth to their management team.

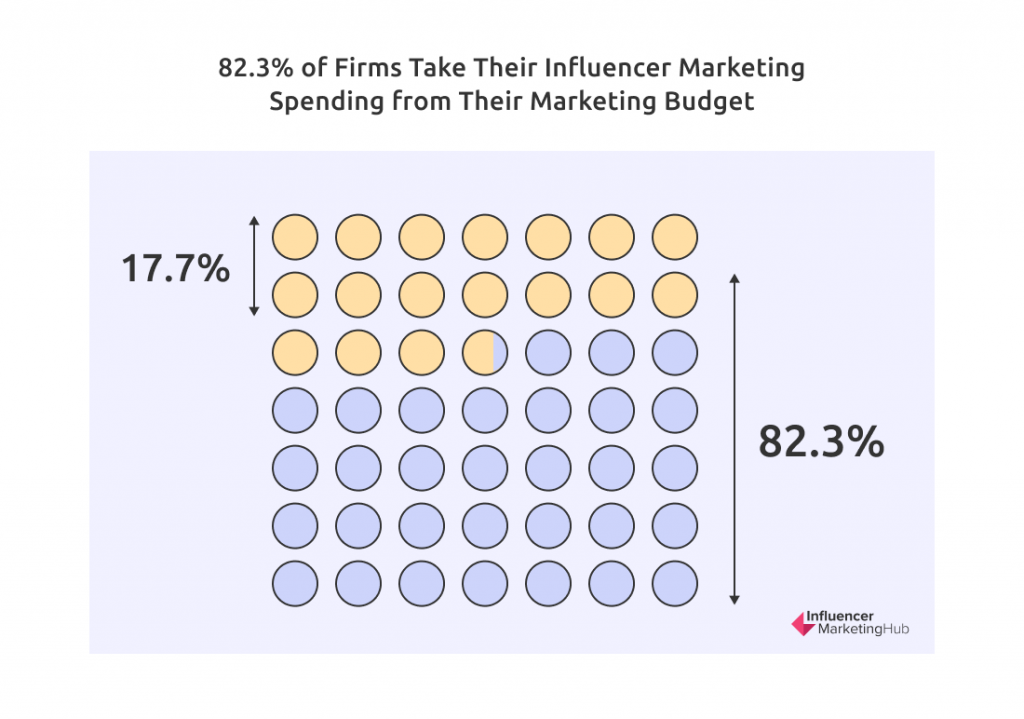

82% of Firms Take Their Influencer Marketing Spending from Their Marketing Budget

This is another statistic showing little change over the last few years. 82.3% of the respondents in our survey take their influencer marketing spending from their Marketing Department’s budget. The remaining 17.7% take their influencer marketing spending from their PR Department’s funds.

Presumably, the firms in the minority group use influencer marketing predominantly for awareness purposes rather than as a direct means to sell their products or services.

71% of Influencer Marketing Campaigns are Run In-House

There has been a small but noticeable change in this statistic this year. With more people working from home, clearly, more firms have decided to outsource their influencer marketing. As a result, 71% of our survey respondents claimed that they ran their influencer campaigns in-house (down from 77%), with the remaining 29% opting to use agencies or managed services for their influencer marketing (up from 23%).

In the past, firms found influencer marketing challenging because they lacked the tools to facilitate the process – organic influencer marketing can be very hit-and-miss, making it frustrating for brands trying to meet their goals. However, many firms now use tools (whether in-house or from third parties) to facilitate the process.

Some brands prefer to use agencies when working with micro and nano-influencers because the agencies are more experienced at working with influencers at scale. Also, larger firms use agencies for all of their marketing, including influencer marketing.

Half of Respondents Use Tools Developed In-House to Execute Influencer Marketing Campaigns

This year, a new question asked our respondents whether they used any tools developed in-house to execute their influencer marketing campaigns. The result was that almost half (49.9%) admitted to using their own tools.

Just Less Than Half of All Respondents Use 3rd-Party Platforms

When asked whether they use 3rd-party platforms to assist them with their influencer marketing, 44.6% said they did. This doesn’t precisely match the results of the previous question – you can’t say that firms either develop tools internally or use a platform (but the results correlate to a substantial degree).

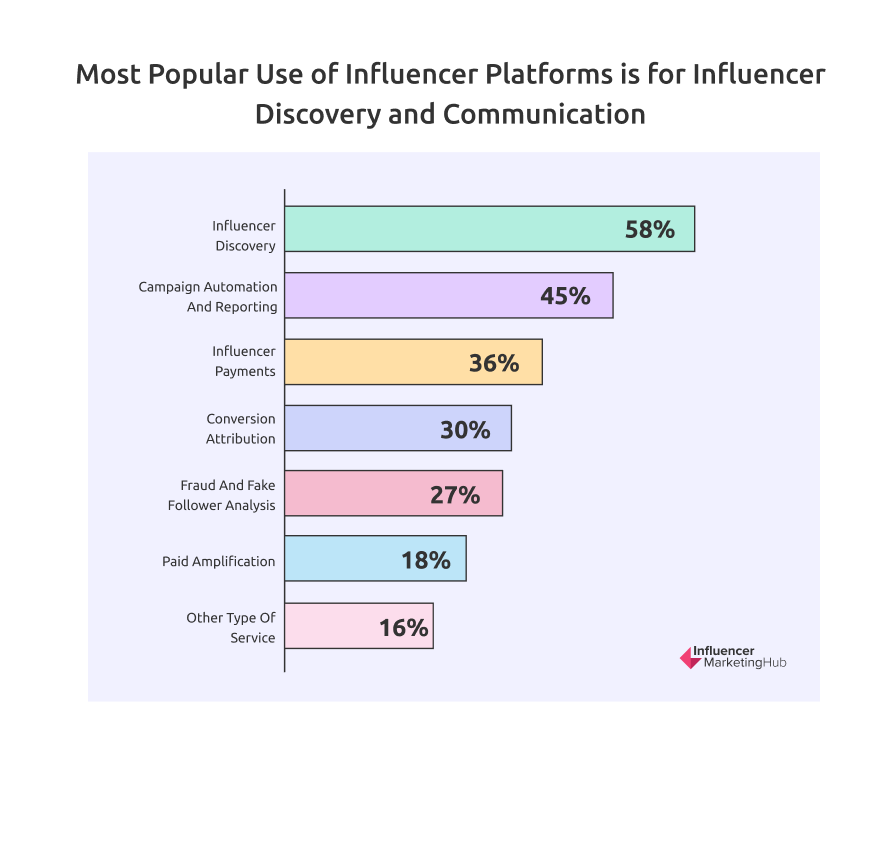

Most Popular Use of Influencer Platforms is for Influencer Discovery and Communication

The figures in this section show a percentage of those who answered that they use a third-party platform, not the percentage of all survey respondents as a whole.

Influencer platforms initially focused on offering tools to help with influencer discovery. Therefore, it should be no surprise that that is still the most popular use of influencer platforms at 58% (up slightly from last year’s results).

Other popular uses of the influencer platforms include campaign automation and reporting (45%), influencer payments (36%), conversion attribution (30%), fraud and fake follower analysis (27%), and paid amplification (18%). An additional 16% of respondents use the platforms for some other type of service.

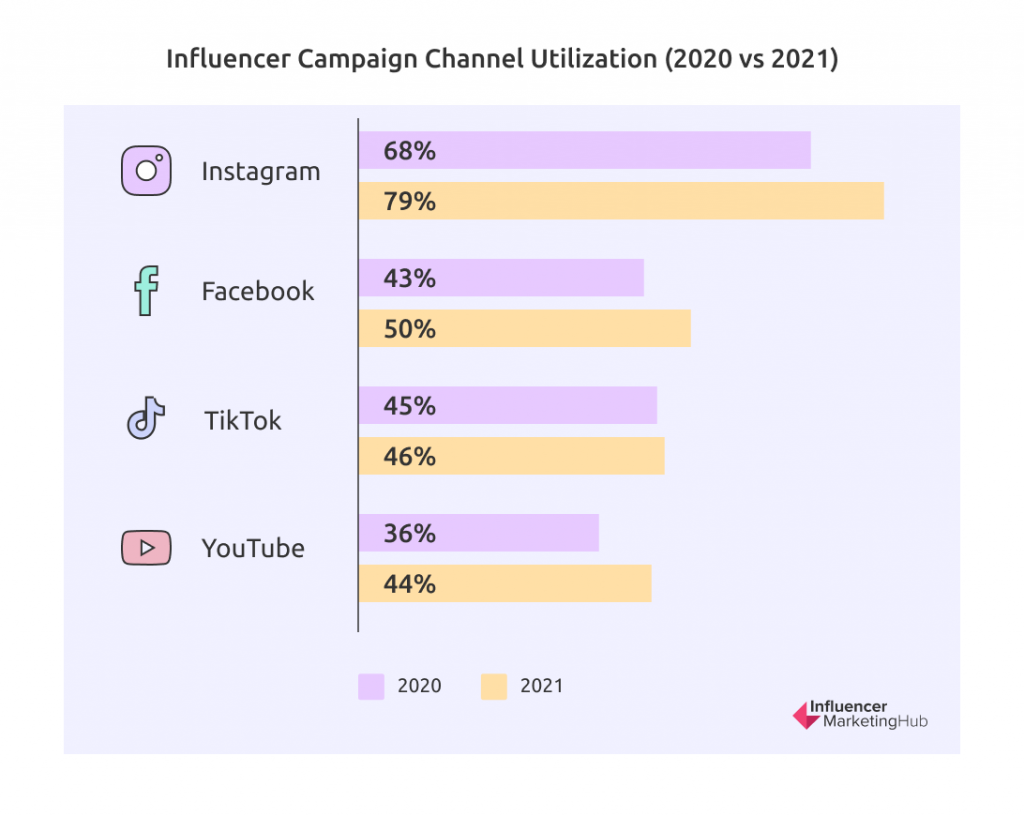

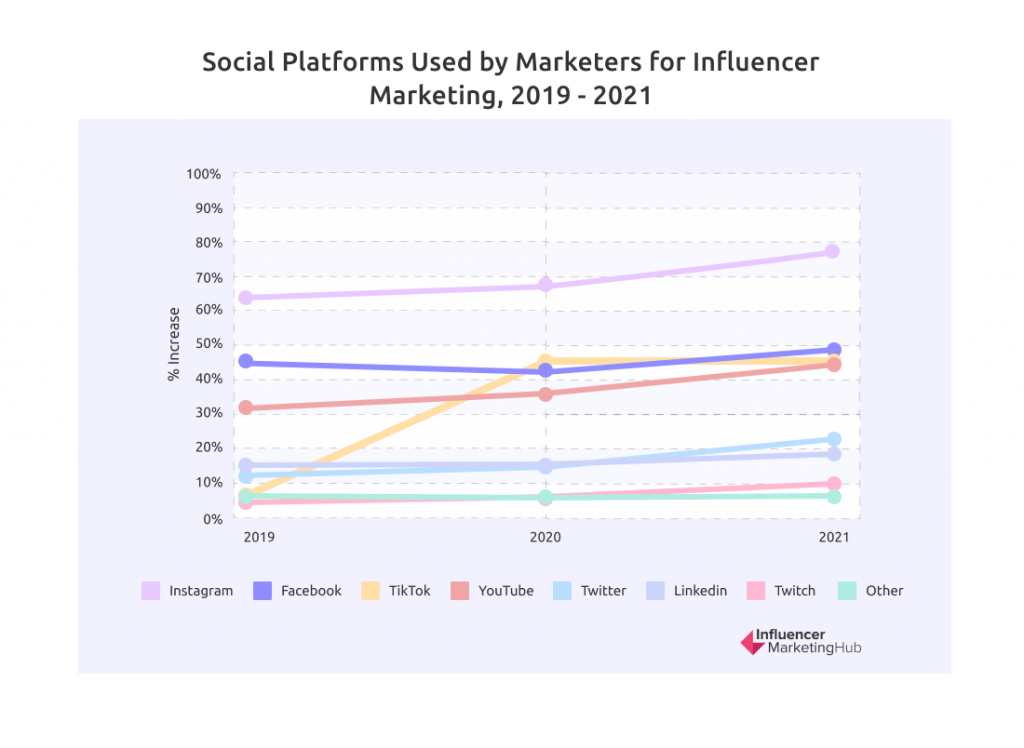

Instagram Used by Nearly 4/5 of Brands Who Engage in Influencer Marketing

Instagram remains the network of choice for influencer marketing campaigns. After a noticeable reduction in use last year to 68%, Instagram improved its popularity over 2021 and was used by 79% of our respondents for influencer marketing.

Last year we saw a significant increase in the use of TikTok (rising from merely being lumped in “Other” in 2020 to 45% usage in 2021. This year it kept its popularity, rising slightly to 46%, but it dropped a position to third.

Surprisingly, Facebook jumped in popularity as an influencer marketing channel last year, with 50% of brands working with Facebook influencers. Facebook doesn’t have as many high-profile influencers as its more visual counterparts, but it is still popular, particularly with older audiences. Perhaps brands have been targeting older Millennials, Generation X, and Baby Boomers more this year with their influencer marketing.

The percentages using the other social channels have increased slightly compared to last year. For example, 44% of the respondents tap into YouTube for their campaigns (36% last year), 23% Twitter (15% last year), 20% LinkedIn – presumably those involved with B2B companies (16% last year), 11% Twitch (8% last year) and a further 7% spread across the less popular or more specialist social networks (6% last year).

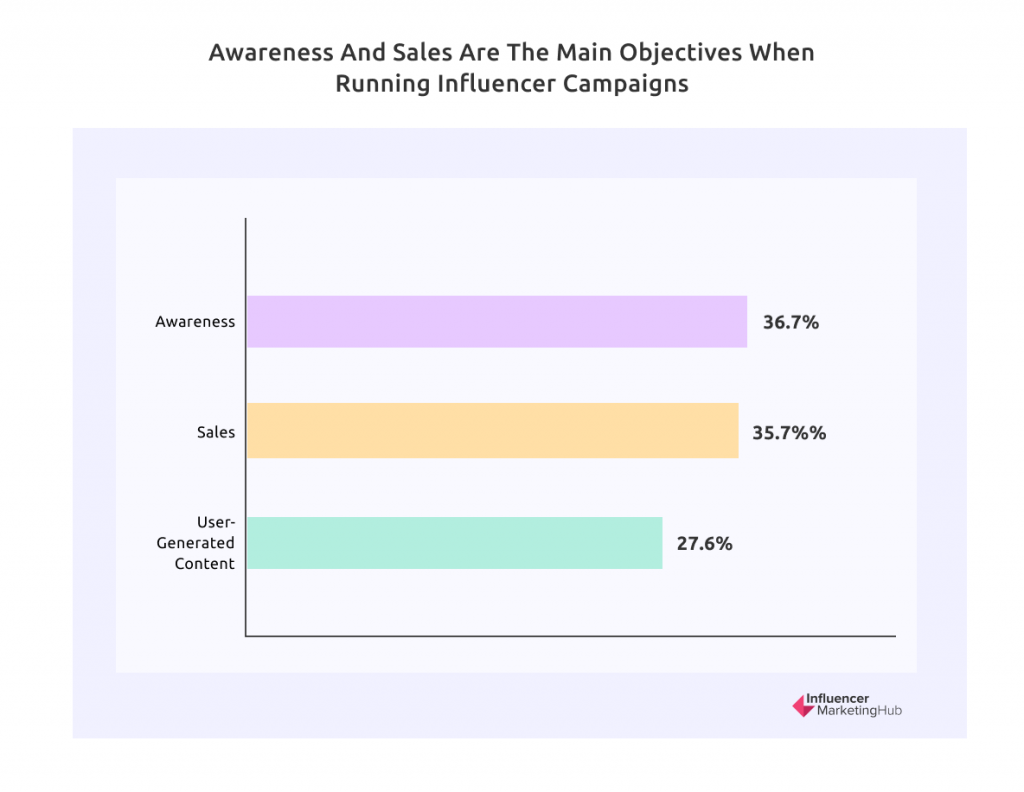

Awareness and Sales are the Main Objectives for Running an Influencer Campaign

Once again, increased sales are the main objective for running an influencer campaign, but awareness is almost equal.

36.7% of our respondents claim their influencer campaign aims to increase sales (up from 33.6%). 35.7% place more emphasis on awareness (also up, from 33.5%). Less popular this year, at 27.6% compared to last year’s 32.8%, is the group of respondents who engage in influencer marketing to build up a library of user-generated content.

Influencer Fraud is Still of Concern to Respondents

Every so often, mainstream media highlights influencer fraud. Luckily there are many tools to help detect fraudsters, reducing the effects of influencer fraud. Hopefully, it will soon merely be a chapter in the industry’s history.

However, influencer fraud has not been wholly vanquished from brands’ and marketers’ minds yet. There has been less publicity about influencer fraud in this Covid era than previously; however, 67% of firms still have worries about the practice.

Several influencer platforms have recognized this area of concern over the last year and have implemented tools to discover and deter influencer fraud.

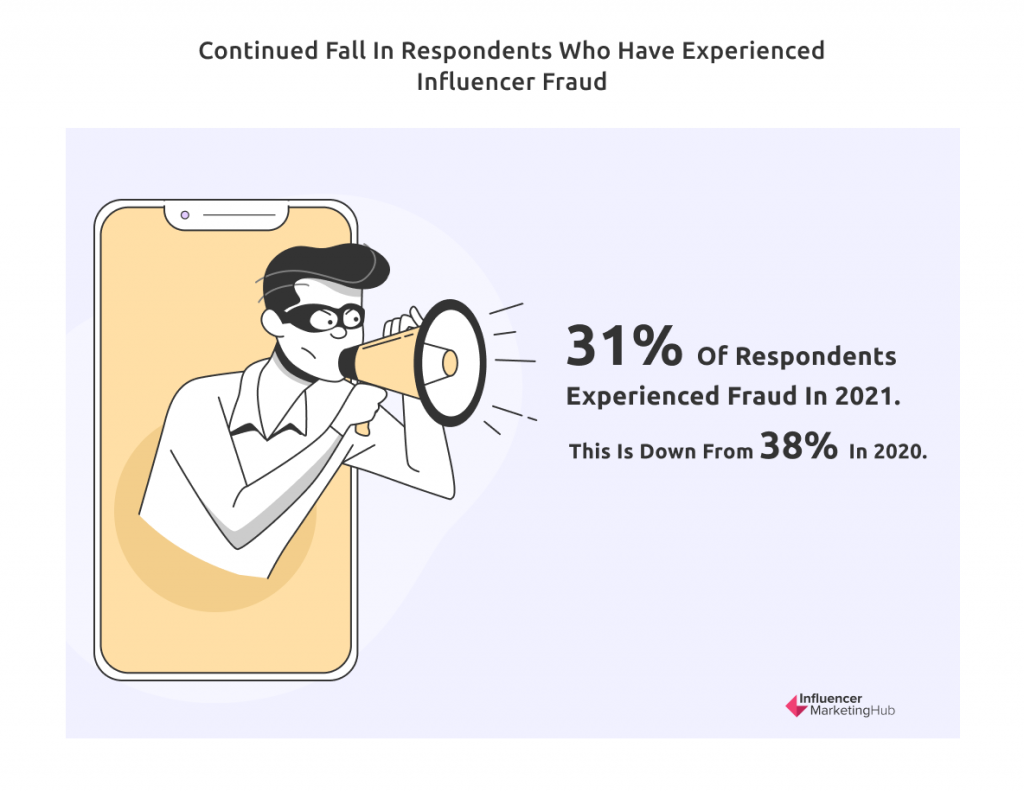

Continued Fall in Respondents Who Have Experienced Influencer Fraud

Despite two-thirds of firms feeling worried about influencer fraud, the number of firms who have experienced it is much smaller. Only 31% of our respondents claim to have experienced fraud, down from the 38% who made this claim a year ago. Widespread publicity about the practice has undoubtedly made businesses warier when selecting influencers with whom to partner.

Brands are Finding it Relatively Easy to Find Appropriate Influencers

This is one of those questions that result in frustrating answers. Those claiming to find it very difficult to discover influencers have dropped from 22% to 16% this year. However, the percentage claiming to find it easy has also fallen, from 22% to 16%. As a result of these conflicting statistics, we now have many respondents (63%) describing the difficulty of finding appropriate influencers with whom to work in their industry as being “medium.”

Perhaps the best way to look at this statistic is that 79% don’t consider it very difficult to find appropriate influencers. This suggests that brands benefit from having more platforms and other influencer discovery tools available than ever (as well as influencer agencies for those wishing to outsource the entire process). Firms frequently reuse influencers with whom they have worked in the past. Some brands still struggle to find suitable influencers, however, perhaps because they are unwilling to pay for the relevant tools or platforms.

This statistic suggests that influencer platforms still need to do a better job marketing their services. In addition, there are still potential customers who require assistance at discovering and reaching out to potential influencers.

The Majority of Firms Have Little Concerns About Brand Safety in Influencer Campaigns

A headline-making issue in recent years has been influencers acting in a way deemed inappropriate by the brands they represent. For example, Logan Paul faced criticism over a tasteless video he shared, and brands wondered whether they wanted to continue any connection with him. YouTube had to do significant damage control over the types of videos they allowed and have stricter rules for channels targeting children. TikTok suffered backlash worldwide over concerns about its close ties with the Chinese government, resulting in the Indian government banning the short video app in 2020. The United States made similar threats.

The key to a successful influencer marketing campaign is matching your brand with influencers whose fans are similar to your preferred customers and whose values match your own.

Only 32% of our respondents believe that brand safety is always a concern, although 49% acknowledge that brand safety could occasionally be a concern when running an influencer marketing campaign.

The remaining 19% believe it is not really a concern. Presumably, this last group has mastered the art of finding appropriate influencers for their brands, and they have little concern about a values mismatch.

Majority Believe Influencer Marketing Can be Automated, Although Significant Numbers Disagree

A contentious issue in influencer marketing is the amount of automation you can successfully use. Some people believe you can automate virtually everything from influencer selection to influencer payment. Others value the personal touch and think influencer marketing is a hands-on process.

The majority of respondents (56%, unchanged from last year) believe that automation plays a vital role in influencer marketing.

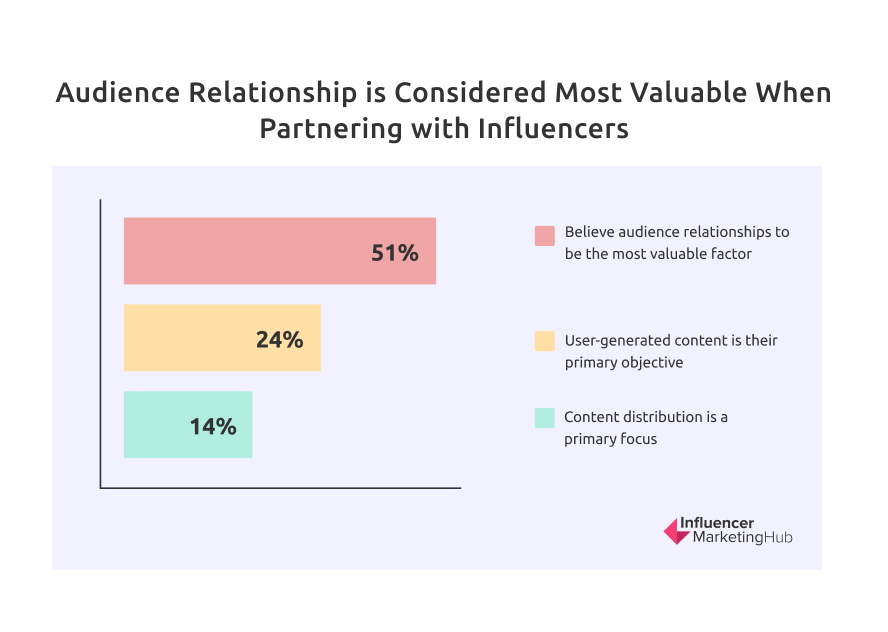

Audience Relationship Still Considered Most Valuable When Partnering with Influencers, But Content Production is Rapidly Catching Up

51% of the survey respondents believed audience relationship to be the most valuable factor when considering collaborating with a particular influencer. This is up on last year’s 45% and indicates a return to views expressed in 2020. Our respondents see little value in working with somebody who doesn’t really influence their audience or perhaps has an excellent relationship – but has the wrong audience for that brand.

The second most important factor is content production at 24% (noticeably down from last year’s 34%). This will be particularly relevant to the group that considered user-generated content their primary objective when running an influencer campaign in our earlier question on influencer campaign objectives.

The third popular reason favored by just 14% of our respondents (down from 22%) found for working with influencers is distribution. Although this is lower than the other options, it connects with audience relationships – influencers use their audience to distribute content relating to a brand.

This year, a new suggestion was attribution and tracking, which 6% of our respondents considered most valuable when partnering with influencers. This ties in with the increased importance of influencers generating sales for their partner businesses.

More Than 70% of Respondents Prefer Their Influencer Marketing to be Campaign-Based

We have seen that brands prefer cultivating long-term relationships with influencers. Yet, brands still think in terms of influencer marketing campaigns. Once they complete one campaign, they plan, organize, and schedule another one. Brands find that influencers they have worked for on previous campaigns are more genuine. Despite this, a massive 72% of influencer marketing relationships are campaign-based, with only 28% “always on.”

This could represent more brands entering the industry, dipping their toes in the water before making long-term commitments to influencers. Alternatively, they may run multiple campaigns, selecting a preferred selection of influencers for each campaign, depending on the target market. Time will tell whether the nature of brand-influencer relationships changes in any significant way.

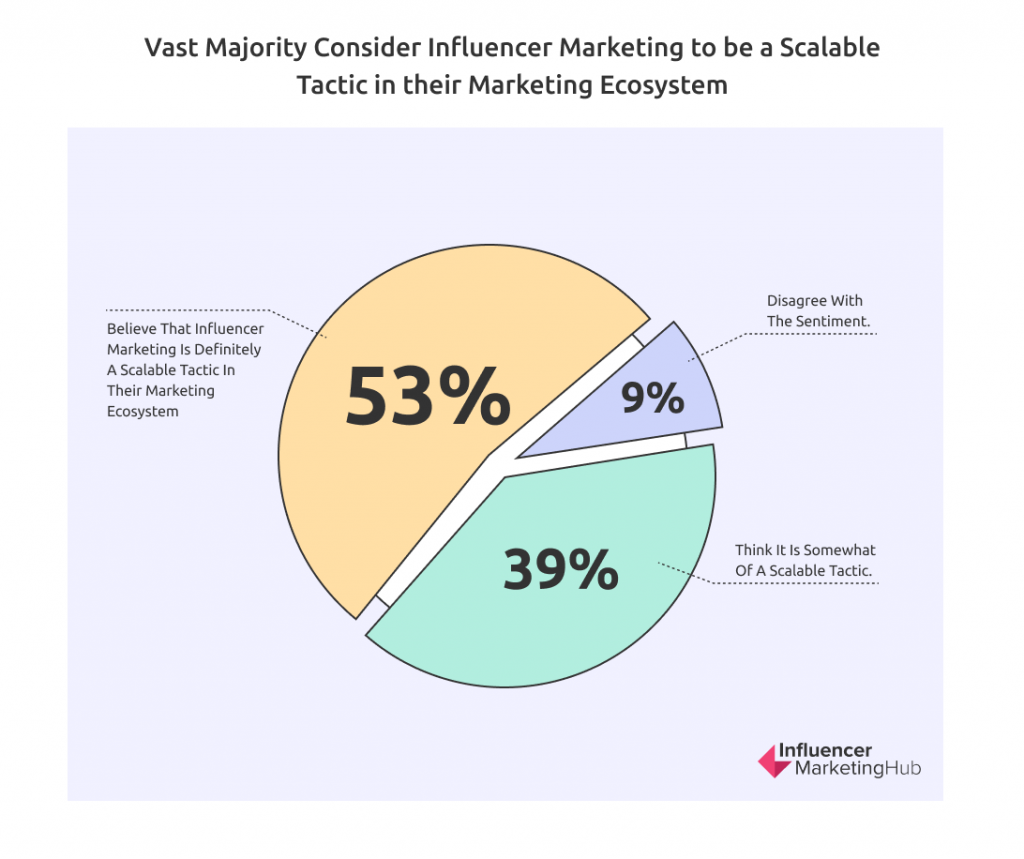

Vast Majority Consider Influencer Marketing to be a Scalable Tactic in their Marketing Ecosystem

One of the most significant advantages of influencer marketing over social activity using official company accounts is the ease of scaling the activity. If you want to create a more extensive campaign, all you need to do is work with more influencers, particularly those with larger followings – as long as they remain relevant to your niche.

While organic influencer marketing may be challenging to scale because of the time needed for influencer identification and wooing, there are now approximately 18,900 Influencer Marketing related services/companies worldwide that businesses can use to help scale their efforts. Many of these operate globally and accept clients from anywhere in the world.

53% of our respondents believe that influencer marketing is definitely a scalable tactic in their marketing ecosystem, and a further 39% think it is somewhat of a scalable tactic. Only 9% disagree with the sentiment. The vast majority recognize that influencer marketing is, to some extent, a scalable tactic in their marketing ecosystem.

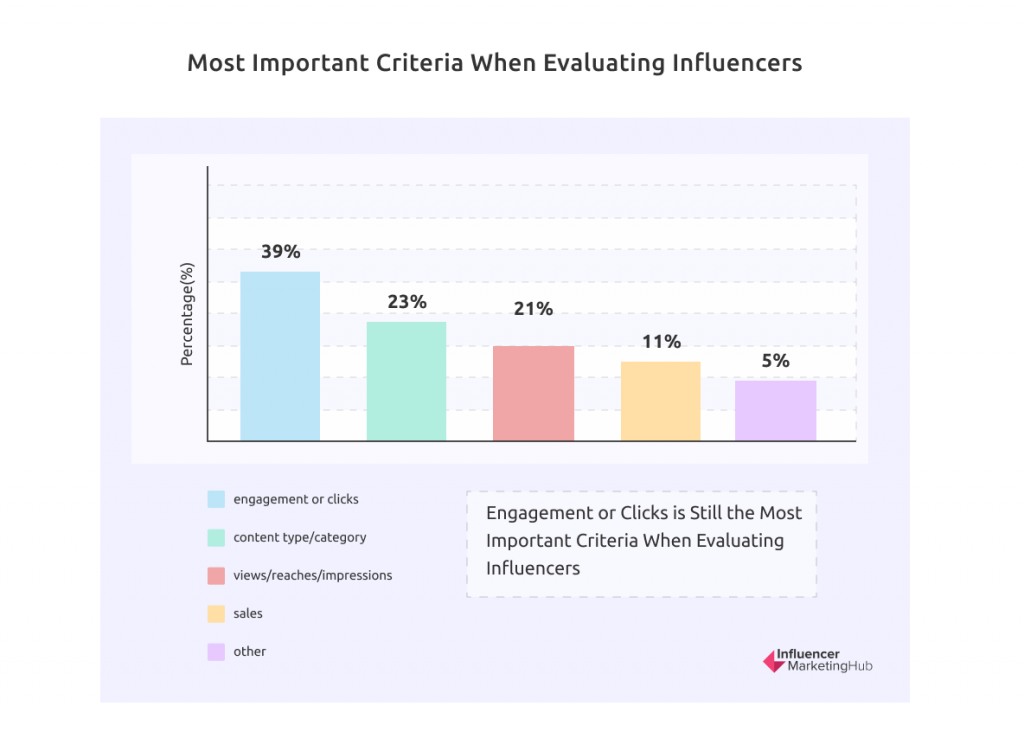

Engagement or Clicks is Still the Most Important Criteria When Evaluating Influencers

We have regularly seen that businesses have a variety of objectives when they create influencer marketing campaigns. While the criteria by which our survey respondents evaluate influencers do not precisely match their differing goals, there is some clear correlation.

39% of our respondents rated engagement or clicks as their most important criterion (the same as last year). The next two categories have switched positions this year, back to how they were in 2020. 23% opted for content type/category (compared to 24.5% last year), while 21% consider views/reach/impressions to be the most important (28% last year). Sales warrants its own category this year, with 11% support. The remaining 5% of the respondents have different ideas on this topic, opting for Other as the most important criterion when evaluating influencers.

Although only 23% claim that content type/category is the most important criterion, this percentage may be understated. Most brands start their influencer search by narrowing down the possibilities to just influencers in a particular niche – a beauty brand is unlikely to work with a home improvement influencer, no matter how engaged he is with his followers. Similarly, it would be unwise for an automotive dealer to opt for a famous beauty influencer, even if she has millions of followers (unless they were promoting a car targeting women).

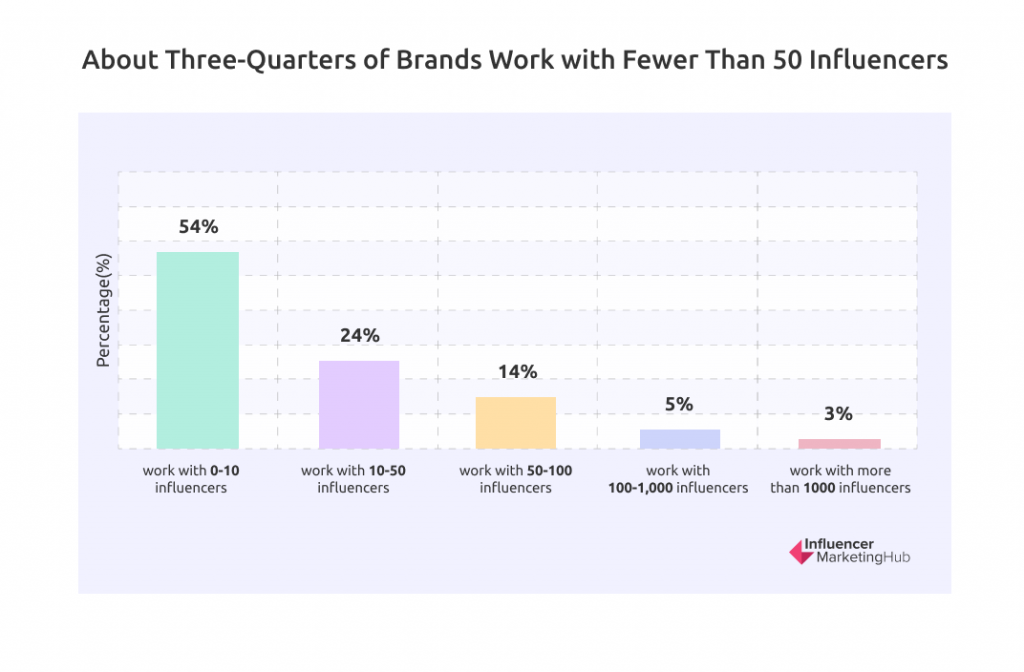

About Three-Quarters of Brands Work with Fewer Than 50 Influencers

We asked those respondents engaged in influencer marketing how many influencers they had worked with over the last year. 54% of them stated that they had worked with 0-10 influencers. A further 24% had worked with 10-50 influencers, meaning 78% of brands worked with fewer than 50 influencers. An additional 14% worked with 50-100 influencers.

Some brands, however, prefer influencer marketing on a large scale, with 5% of those surveyed admitting to working with 100-1000 influencers. A further 3% worked with more than 1,000 influencers. This last figure is half last year’s percentage, but back to how things were in earlier years.

Quarterly Campaigns Are Now the Most Used, Although Monthly Campaigns Are Almost as Common

We have seen a gradual movement towards quarterly campaigns over the last few years, and this year the longer campaign period came out ahead of monthly campaigns.

Of those who operate discrete influencer campaigns, 35% (up from 27%) prefer to run them quarterly. A further 34% (same as last year) run monthly campaigns. Just 14% (down from 17%) prefer to organize campaigns annually. These later companies are probably brands that like the “always-on” approach to influencer marketing. The remaining 18% (down from 23%) take a different approach and only run campaigns whenever they launch a new product.

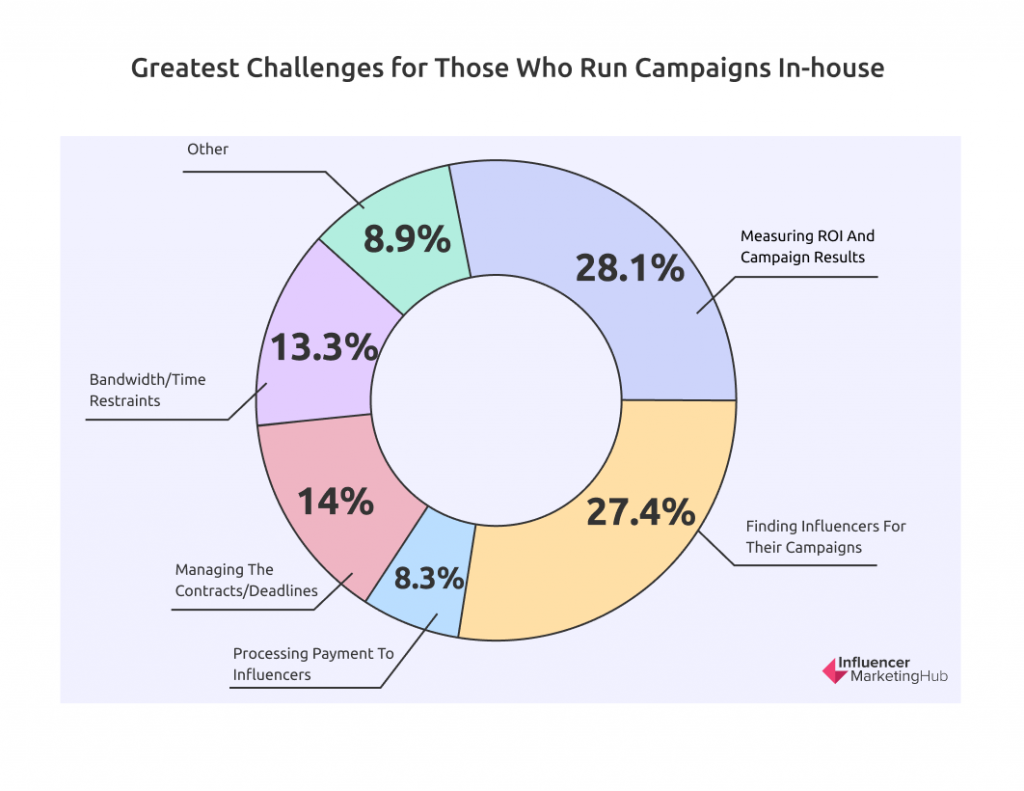

Measuring ROI and Campaign Results is Now the Greatest Challenge for Those Who Run Campaigns In-house

We asked those survey respondents who ran campaigns in-house what they saw as the greatest challenges they faced. This year we saw a change at the top, with 28.1% opting for measuring ROI and campaign results (up from 23.5% last year, the first time it featured separately).

Traditionally, the most significant challenge was finding influencers to participate in their campaigns (27.4% this year). This is down noticeably from last year’s 34%, which was, in turn, a drop from 2020’s 39%. This gradual reduction is probably an indication of increased usage of platforms and other third-party tools.

Other notable areas of concern included managing the contracts/deadlines of the campaign (14%), bandwidth/time restraints (13.3%), and processing payment to influencers (8.3%). A further 8.9% of challenges can be grouped as Other.