It’s just before noon on a Monday in June.

The sky is brilliant blue, the streaks of white clouds betraying no trace of the thunderstorms from the night before, when a tornado touched down near Chicago.

A group of teens huddles around a plot at Alice’s Garden in Milwaukee filled with tidy rows of onions, hot peppers and herbs. A tray of colorful petunias and marigolds sits off to the side.

“Why do we need bees?” asks Shane Woodruff, one of the group’s adult leaders that day.

“To pollinate,” replies 15-year-old Daeshawn Matthews.

Woodruff plucks bits of the herbs, rubs them between his fingers and passes them around the group, asking the teens to smell the aroma and guess what each is. After identifying thyme, rosemary and dill, the group gets to work.

Takiyah Dates, 15, and Emahriyah Jackson, 13, gently loosen purple and pink petunias from their containers and nestle them into the turned-up soil. Later this week, they’ll get their first paycheck.

“Don’t try to spend a lot at once,” Takiyah says of her approach to money. “You buy what you need before you buy what you want.”

Ashley Luthern / Milwaukee Journal Sentinel

The teens are part of an expanded summer jobs program from Running Rebels Community Organization. For many, it’s their first time earning a paycheck, and their mentors want to make sure they learn how to manage money, too.

“If at the end of this, all you got is some new clothes, then we didn’t do our job,” Victor Barnett, the Rebels’ founder and co-executive director, told the group at the start of the summer.

The Rebels’ jobs program joins a growing movement in Milwaukee to boost financial education for kids and teens. Earlier this year, Milwaukee Public Schools added a personal finance course as a graduation requirement, putting it among only a handful of large urban districts in the country to do so.

Ebony Cox / Milwaukee Journal Sentinel

Twenty-one states require high school students to complete a personal finance class to graduate, according to the most recent report from the Council for Economic Education.

Wisconsin is not one of them.

In 2017, state lawmakers did require school districts to adopt financial literacy academic standards. It’s up to each district to decide how to implement them, leading to a wide variation across the state.

In some districts, a teacher trained in personal finance teaches a stand-alone course. In others, the material is sprinkled in economics, business and technology, or family and consumer science classes.

It’s essential that young people get this education, said David Mancl, director of the state’s Office of Financial Literacy within the Department of Financial Institutions.

“People are going to be dealing with money sooner or later in their lives and what they don’t know about money can hurt them,” he said.

Young people can ruin their credit rating before they even know what it is. They might rely on payday lenders or take out high-interest loans without realizing the consequences. They can go online and day trade stocks in minutes, only to lose their money just as fast.

Before they know it, they can find themselves deep in debt and struggling to pay for school, buy the car they need to get to work or qualify for a mortgage.

“The stakes are really high,” Mancl said.

Young people want to learn about money.

Yet nearly one in five 15-year-olds in the U.S. struggles with basic financial concepts, such as simple budgeting and comparison shopping, according to an international financial literacy assessment released last year.

Financial and investment firms regularly release surveys showing most parents feel uncomfortable talking about money.

“Much of that is because they themselves don’t necessarily feel like they are experts in money management,” said Melody Harvey, an assistant professor at the University of Wisconsin-Madison who studies how public policies affect financial capability.

“I imagine that most parents wouldn’t want to intentionally mislead their children or give wrong information,” she said.

The result is that most of the financial education kids get comes in school, whether as part of economics or math courses, or in the form of programming from nonprofit groups that offer investment clubs, financial mentoring for students or in-class workshops.

Carly Urban, an associate professor at Montana State University, studies financial education mandates, identifying states that require students to have some personal finance content before graduation.

“There’s definitely momentum around it,” Urban said of the requirements. “Ten years ago when I started, not many states had policies or were thinking about it. As we’ve developed the research, almost every state has tried to pass something at some point.”

Research suggests those policies make a difference.

One study from economist Daniel Mangrum found that among first-generation or low-income students who had taken such a course, loan repayment was higher, which suggests those students were more likely to have finished college and found a higher-paying job.

Another study found after personal finance education is required, credit scores go up and delinquency rates go down.

A decade ago, Urban and J. Michael Collins, a professor and financial security researcher at the University of Wisconsin-Madison, were part of the team that examined outcomes in Texas and Georgia after those states implemented a financial education requirement.

University of Wisconsin-Madison

They looked at students’ credit reports through age 22 and found students were less likely to have a negative item on their credit report. They also borrowed more — showing they could better fill out applications for things like credit cards or a car loan — and had a lower delinquency rate on those loans than their peers in states without the graduation requirement.

“We saw that those kids who had the financial education had basically fewer mistakes in their early 20s,” Collins said.

States have differing financial education mandates and various levels of support for them, which can affect outcomes, he said.

Wisconsin’s 2017 requirement did not provide widespread funding. Instead, as a way to avoid giving an unfunded educational mandate, the measure gave districts flexibility to incorporate the material based on their finances and staffing. In early 2020, the state offered $150,000 in competitive grants with a maximum $10,000 per school to encourage more personal finance education.

“I would say both Georgia and Texas had some more teeth,” Collins said. “They were much more standardized and they invested millions.”

It’s game day at Running Rebels.

But the competition isn’t in basketball or Ping-Pong. Instead, it’s financial literacy trivia.

About 30 of the youth workers, including Daeshawn, Takiyah and 15-year-old Arrion Carter, are participating. Earlier in the afternoon, they filled out a budgeting worksheet and reviewed key concepts, such as the steps of comparison shopping to find a good deal.

Britney Morgan, the Rebels’ mentor leading the sessions, calls up three boys and three girls for the first round.

“Remember your training!” she says before launching into the first questions.

What is a budget? A budget is something to tell you where you should spend your money. What are taxes? The money that you have to give to the government.

Morgan pauses, calling it a “good teachable moment.” She explains how those who worked their full 20 hours will see $400 listed on their biweekly paycheck, their gross earnings, and their check will be for a smaller amount, perhaps around $350, which is their net earnings.

“Get in the habit of really reading your check stubs and holding onto them,” she says. “You see how your money is flowing.”

Next question: What is a checking account?

Silence fills the room. Morgan calls on Arrion.

“You have a bank account. Sometimes you have a checking account, sometimes you have a savings one,” he answers.

Morgan goes further, reminding the group their checking account is where their spending money goes and is linked to a debit card, while savings accounts mostly have money coming in and staying in the account.

“If you like swiping that plastic,” she says of the debit card, “it will ruin your life if you are not careful. It takes 10 full business days to get a check, it takes two minutes to spend it all.”

Ebony Cox / Milwaukee Journal Sentinel

These lessons are deliberate. Running Rebels has always hired young people, but this summer the organization launched its largest jobs program ever and made financial education a core component. Sixty-seven teens worked 20 hours a week for 10 weeks. Those old enough were paid $10 an hour, while those 12 to 14 years old received a stipend of $8 per hour.

They tended community gardens, cleaned up parks and staffed tables with COVID information during pop-up neighborhood events, all under the supervision of Rebels staff.

“Our goal is to use people from the community, and empower them to mentor people from their own community,” said Dawn Barnett, Running Rebels’ co-executive director.

The challenges faced by staff are the same faced by the wider community. So when she noticed garnishments while processing payroll for a few staff members, she and Victor Barnett, her husband, organized financial education workshops for employees before the summer started.

“Being financially unhealthy seeps into your physical wellness, emotional, mental states of mind,” she said.

The teens at Running Rebels go to public and private schools across the metro area.

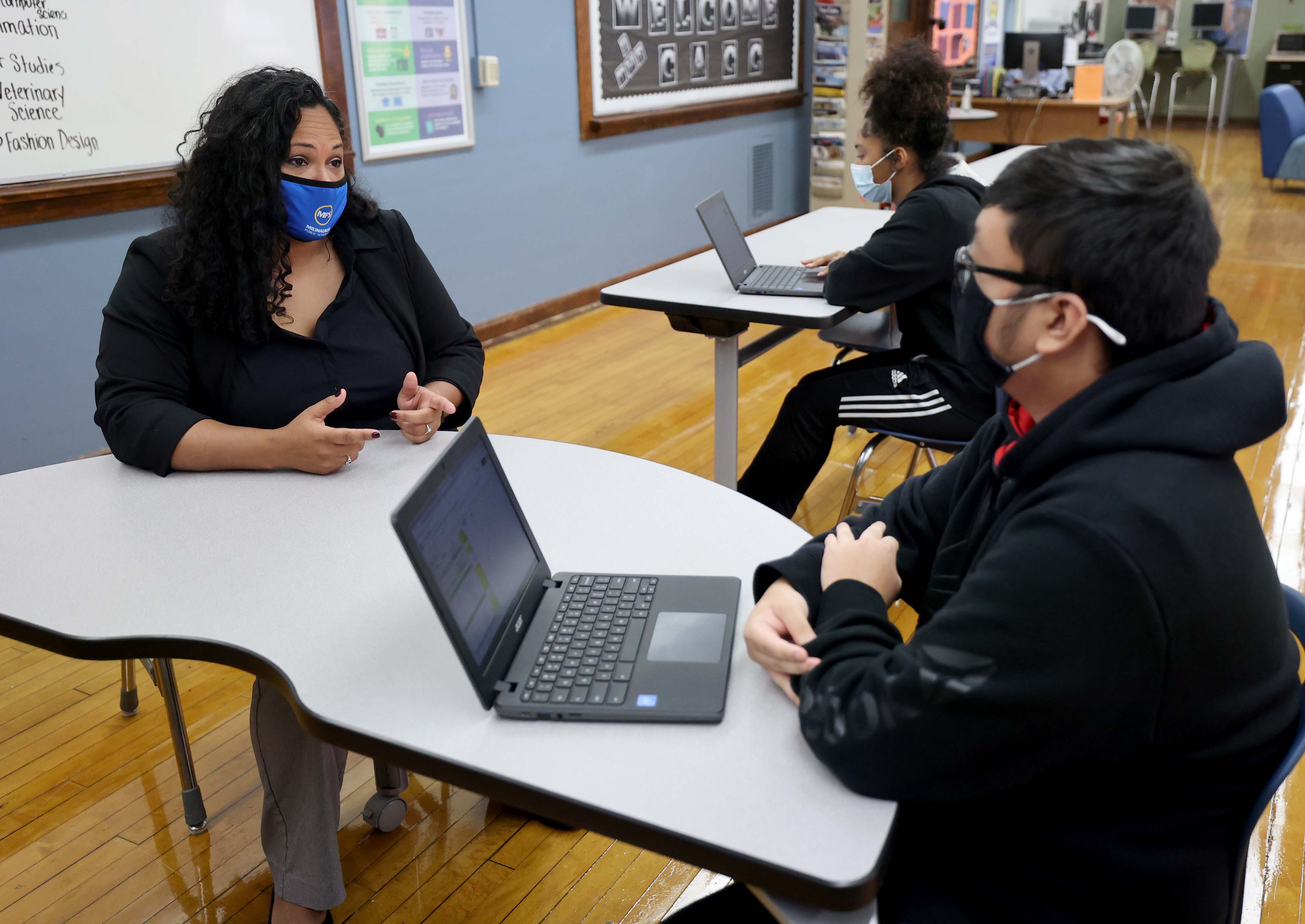

Those who are 12 and attend Milwaukee Public Schools will likely have the chance to take a personal finance course, under new requirements passed this year.

MPS is phasing in the new personal finance graduation requirement starting with three high schools, Riverside, Hamilton and GreenTree Prep. The semester-long course covers budgeting, checking and savings accounts, paying for college, credit management, investing, insurance, taxes and behavioral finance. Right now, the course is offered as an elective, but will be a graduation requirement for the class of 2026 at those schools and is expanding to 13 more schools next semester.

“Having a personal finance course opens the gateway for financial freedom,” said Marti Diaz, MPS’ financial literacy teacher mentor who is the course instructor.

Among the 477 students taking the class this fall, 75% are considered economically disadvantaged and 60% are Black, 24% are Hispanic, 19% are Asian, 3% white and 1% are multiracial.

“We talk about the history of racism in banking, the fact that there’s some predatory lending in our communities,” Diaz said.

The district plans to launch the curriculum at its remaining high schools with the last cohort starting in spring 2023. Prior to this, students “had access to personal finance education,” which had been “embedded in other courses and taught with a variety of instructional resources,” according to a presentation this fall to the board.

The district has contracted with Secure Futures, CLIMB USA and Junior Achievement to provide some personal finance lessons, but those often were units within larger courses or workshops. Fund My Future Milwaukee, which aims to open a 529 college savings account for every 5K student, also has provided financial literacy lessons at participating schools.

Now, MPS will have teachers trained on the standalone curriculum. The effort is backed by a three-year $490,000 grant from Next Gen Personal Finance, a national financial literacy nonprofit, to pay for Diaz’s salary and benefits and other program costs. The state Department of Financial Institutions with support from the Department of Public Instruction also contributed $30,000 in grant money and the district has used some COVID relief funding, too.

Mike De Sisti / Milwaukee Journal Sentinel

Tim Ranzetta, Next Gen’s co-founder, is an evangelist for personal finance education as a standalone course, rather than included in economics or other classes where teachers already have a lot of material to get through.

“It doesn’t work if it’s embedded in another course,” he said.

Others have argued it’s better to have some financial education, even if it is spread across other subjects, rather than none at all or forcing teachers who aren’t trained in the subject to teach it.

About one-third of Wisconsin’s high schools publish public online course catalogs. Using that information, Urban found about 43% of those 271 schools required students take a standalone financial course in the 2020-21 academic year. Another 44% offered a standalone course, while just over 10% had it embedded in other courses. Fewer than 2% did not offer the material.

Nationwide, about one in five high-schoolers are guaranteed to have access to a personal finance course. But for districts that predominantly serve Black and brown students, the number plummets to 1 in 14, according to research funded by Next Gen.

To Robert Wynn, a former financial education officer at the Wisconsin Department of Financial Institutions, those statistics reinforce the importance of financial education as a matter of social justice.

Wynn has made it his life’s work to teach young people of color about investing and stocks through Asset Builders and CLIMB USA, which has provided investment education in MPS and activities for Running Rebels.

“If we just dealt with policy issues on incarceration, inequality, or even police brutality, you really don’t get to the core issue, which is power,” Wynn said.

“And power really does come from wealth in this country.”

It’s the last day of the Running Rebels jobs program and time for awards.

Daeshawn, whose favorite work site was Alice’s Garden, is honored for having earned the most points this summer for attendance, taking part in extra activities and having a good attitude.

He’s one of four teens asked to come onstage and take a turn at the microphone. The most important thing he learned, he says, is communication.

Ebony Cox / Milwaukee Journal Sentinel

Of the 67 youths who started the 10-week program, 61 finished and received a bonus $150 savings stipend for their newly opened bank accounts. United Way of Greater Milwaukee and Waukesha Counties provided $100,000 in funding for wages, saving incentives and supervision.

Takiyah, who happened to be in Daeshawn’s group, also is called up for an award for her “diligence.” This summer boosted her confidence, she says.

She opened her first bank account as part of the summer program after learning about the high fees of check-cashing operations.

“I learned that it’s best to save and not to spend all at once, and that even though you might want a lot of stuff, it’s not best to get it right then and there,” she said. “It’s best to get what you need first.”

She’s saving much of her summer earnings for college.

“This shows that I can do it,” she said. “I can work, and I can make my own money and I can do what I need to do financially for myself.”

Next Gen Personal Finance offers free online games for people of all ages. Can you make it through a month living paycheck to paycheck? Find out using Spent. Want to see the consequences of 20 years of investing over 20 years? Check out Stax. All games are available online at ngpf.org/arcade.

Running Rebels Community Organization is built on mentoring. There are opportunities for young people to get involved, for adults to mentor and for supporters to donate or contribute by purchasing items off the group’s wish list. Details available online at runningrebels.org.

Asset Builders and CLIMB USA provide investment workshops inside and outside the classroom, and other opportunities for young people and adult volunteers. More information is at assetbuilders.org and climbusa.org.

Secure Futures connects educators and volunteers to provide in-class financial capability instruction with participating schools. To learn how to get involved, go to securefutures.org.

Contact Ashley Luthern at [email protected]. Follow her on Twitter at @aluthern.