The digital revolution has changed the world in just the last decade and a half, spawning new technologies, new ways of using technologies, and bringing old businesses into the 21st century. Nowhere is this more obvious than in the financial sector. Banking and financial services have benefited enormously from bringing tech into the mix – and their gains have given us a new word to describe it, fintech.

5-star analyst Jeff Cantwell, of Wells Fargo, lays out the upside case for fintech in no uncertain terms: “We see a $1.5T annual revenue opportunity for Fintech companies globally, and expect 6% annual growth over the ensuing decade… Now is a highly opportune time for investors to take a fresh look at Fintech given current valuations. We expect that these companies’ fundamentals will strengthen in ’22/’23 and that the group’s current discount to the broader market will not hold.”

Against this backdrop, Cantwell has pinpointed 2 fintech stocks which he believes are set to push ahead over the coming months. And he’s not alone in his bullish outlook. According to TipRanks database, both tickers carry a Strong Buy consensus rating from the rest of the Street. Let’s take a closer look.

Paymentus Holdings (PAY)

First up is Paymentus, a bill payment fintech firm offering cloud-based solutions as an omni-channel integrated payment platform. The company’s product line delivers the latest in payment management tech to more than 1,700 billers and financial institutions. One figure will show the magnitude of Paymentus’ market: in 2021, the company cleared more than 280 million payment transactions.

Paymentus went public in May of last year, putting 10 million shares on the market at a price of $21 each and raising more than $210 million in gross proceeds. The stock has tumbled ~42% thus far in 2022, and now trades slightly below its IPO price.

That loss came even as the company reported sound financial results. Paymentus released its first set of results for 2Q21, and showed $93.5 million in revenue. That increased to $101.6 million in 3Q21, and in the most recent quarter, 4Q21, it increased again to $108.1 million. The 4Q number was up 31% year-over-year. In its core business, processing payment transactions, Paymentus showed clear growth in Q4. The company handled 83.3 million transactions, up ~54% year-over-year.

For the full year 2021, Paymentus brought in $395.5 million in revenue, up ~31% from 2020. The company reported having $168.4 million in cash on hand at the end of 2021.

Cantwell sees a clear path forward for this company, for two reasons – first is Paymentus’ quality, and second is the known waste in its niche. The analyst writes: “We view Paymentus as a ‘next-gen’ disruptor, and we expect it will gain further share over the next two years as the company continues to execute in a space (bill payments) that is otherwise characterized by inefficiency. The natural consequence of these share gains by Paymentus will be strong expansion in the firm’s revenue and adjusted gross profit… . Longer term, we also believe Paymentus will expand adjusted EBITDA margins and drive improved profitability as it further consolidates its leading position in bill payments.”

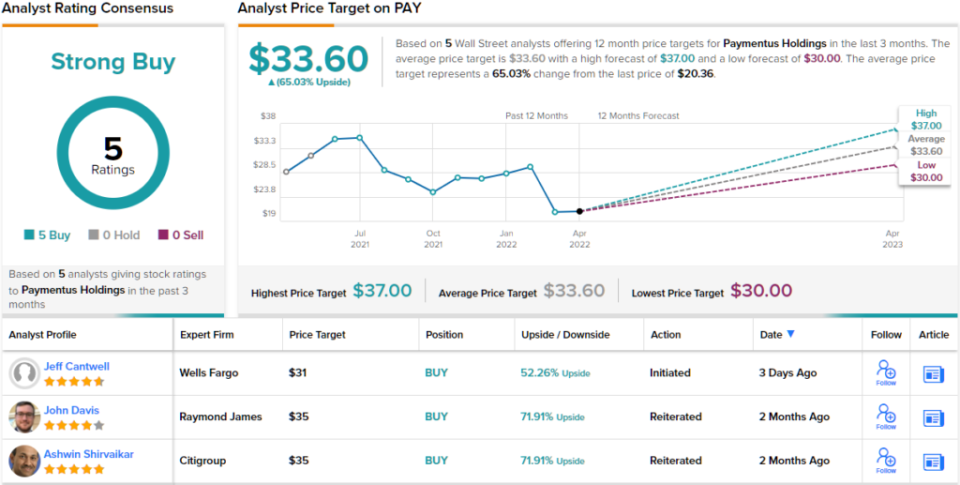

To this end, Cantwell initiated coverage on Paymentus shares with an Overweight (i.e. Buy) rating and a $31 price target. Investors are looking at one-year gains of 52%, should Cantwell’s forecast go according to plan. (To watch Cantwell’s track record, click here)

It’s clear from the analyst consensus that the Street agrees with this bullish take. Paymentus has 5 positive reviews, making the Strong Buy consensus rating unanimous. The shares are trading for $20.36 and their $33.60 average target implies a 65% upside from that level. (See Paymentus stock forecast on TipRanks)

Global Payments (GPN)

The second Wells Fargo pick we’re looking at is another payment processor – but where Paymentus is focused on the North American market, Global Payments reaches worldwide. The company boasts 4 million customers in more than 100 countries; it provides seller services, offering payment technology to merchants to process credit cards, debit cards, digital payments, and even the new contactless payments. Global Payments handles more than 50 billion transactions every year.

In February of this year, Global Payments reported its Q4 and full year results for 2021, and showed records on both counts. For the quarter, the company had $2.19 billion in revenues, up 13% year-over-year, along with diluted earnings of 72 cents per share, up 18% from the prior year fourth quarter.

Looking at the full year of 2021, the company’s top line came to $8.52 billion. Compared to the $7.42 billion in 2020, this was ~15% gain. Diluted EPS for 2021 was $3.29, up a robust 68% from $1.95 in 2020.

Global Payments has a firm foundation, a fact noted by Cantwell in his initiation of coverage report. The analyst points out the company’s obvious strengths – its global reach, it’s high revenues – and writes, “We expect GPN to compound EPS rapidly over the next two years as it increasingly amplifies its leadership positions across both payments and software… We expect strong firmwide financial results on solid top-line performance (revenue growth: 9% in both ’22/’23), driven by Merchant Solutions, where we see low-double-digit topline growth in ’22/’23 on continued strong performance in North America.”

“Bottom line, we think GPN is undervalued at current levels. Risk/reward looks favorable to us here,” the analyst summed up.

In line with this bullish stance, Cantwell rates the shares an Overweight (i.e. Buy) and gives them a $194 price target that indicates confidence in a 39% one-year upside.

Overall, this global company has picked up 15 analyst reviews in recent weeks and they break down 13 to 2 in favor of Buys over Holds, for a Strong Buy consensus rating on the Street. GPN carries an average analyst price target of $188.14, implying ~35% upside from the current trading price of $138.90 over the next 12 months. (See GPN stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.