The 1st 50 % of 2022 was marked by fears about inflation, rising interest prices and economic downturn, with the S&P 500 registering its worst 50 % calendar year due to the fact 1970.

On the other hand, not all people is observing dark situations forward. Marko Kolanovic, head of world wide markets system for JPMorgan, thinks that existing problems may perhaps also be a established-up for a rebound in the second fifty percent of the yr, specifically among the the little-cap shares. Kolanovic writes of this case, “If there is no economic downturn – which is our view – then risky asset price ranges are far too low cost. For instance, modest cap stocks in the US at this time trade in the vicinity of the least expensive valuations at any time.”

If Kolanovic is right, and we’re hunting at a opportunity rebound in the tiny-cap sector, then the organic reaction for buyers would be a move towards the ‘pennies,’ the stocks priced underneath $5 per share. Though not always a certain indicator, very low share cost normally goes hand-in-hand with lower marketplace cap – but it also arrives with the stable upside opportunity, as even little gains in complete terms can speedily turn into substantial-percentage increases in share selling price.

That reported, right before jumping proper into an investment in a penny inventory, Wall Road professionals recommend wanting at the larger photograph and taking into consideration other elements past just the selling price tag. For some names that slide into this category, you definitely do get what you spend for, supplying small in the way of extended-expression growth prospective buyers many thanks to weak fundamentals, modern headwinds or even substantial remarkable share counts.

Using the possibility into consideration, we used TipRanks’ databases to discover two persuasive penny stocks, as determined by Wall Avenue execs. Just about every has attained a “Strong Buy” consensus rating from the analyst neighborhood and brings substantial growth prospective customers to the desk. We’re chatting about in excess of 200% upside opportunity listed here.

Codiak BioSciences (CDAK)

We’ll commence with Codiak BioSciences, a medial study business working on new therapeutics agents for the cure of a extensive variety of illnesses that have in popular high ranges of unmet clinical requirements. Codiak’s principal study focus is on exosomes, or the RNA degradation system, and the thrust of the investigation is to develop a course of medications that use exosomes to transfer genetic materials for a therapeutic influence.

The corporation presently has three drug candidates in clinical trials, all in early phases of testing. All a few are below investigation as therapies for cancer. The two more advanced candidates, exoIL-12 and exoSTING, therapies for cutaneous T-cell lymphoma and good tumors respectively, have the two shown ‘favorable protection and tolerability profiles’ in Period 1 trials, which commenced in September of 2020. This past June the company launched facts on each trials showing clinically important success, and justifying further scientific studies. Codiak designs to initiate Phase 2 trials on equally tracks in 1Q23.

On the third clinical observe, the drug candidate exoASO-STAT6 started Section 1 scientific trials before this yr and the business announced the initiation of patient dosing at the end of June. The drug is getting investigated as a therapy for myeloid loaded cancers, and this trial will focus on creating a tolerability and safety profile to determine the suitable dosing for afterwards research. Original info is expected to be introduced all through 1H23.

Codiak has various preclinical tracks underway, in addition to these scientific scientific studies. The most outstanding of the preclinical investigate applications is remaining carried out with CEPI, the Coalition for Epidemic Preparedness Innovations, and is a broadly protective vaccine application as a prophylactic versus SARS-CoV-2, the virus family members leading to COVID-19.

Whilst Codiak shares have taken a strike 12 months-to-date, at $2.82, several analysts imagine the price tag signifies a distinctive obtaining possibility.

Amid the bulls is David Nierengarten, 5-star analyst with Wedbush, who sees the recent scientific details as the key element to look at. He writes, “We consider the information presented even further validates CDAK’s exosome system and has de-risked two of its therapeutic candidates, which we view as greatest-in-class molecules. With three systems in the clinic, two data catalysts anticipated over the up coming 12 months (last dose escalation knowledge for exoSTING in 4Q22 and original exoASO-STAT6 facts in 1H23), and an EV of $50-60MM, we see a favorable hazard/reward for CDAK.”

In line with his bullish stance, Nierengarten prices CDAK a Buy, and his $17 cost concentrate on implies room for an amazing 513% upside to the shares about the next 12 months. (To check out Nierengarten’s keep track of history, simply click listed here)

What does the rest of the Avenue believe about CDAK extended-phrase prospective clients? All of the other analysts that have thrown an impression into the blend not too long ago see the stock as a Obtain, generating the consensus score a Robust Acquire. Centered on the $11 average cost focus on, the upside possible lands at 289%. (See CDAK stock forecast on TipRanks)

Olema Prescription drugs (OLMA)

The second penny we’ll seem at is Olema, an early-stage biopharmaceutical analysis business with a concentrate on estrogen-joined cancers. The enterprise is performing on the discovery, advancement, and lengthy-term commercialization of estrogen receptor antagonist drug candidates, as therapeutic brokers for cancers unique to women. Olema’s prime drug prospect software, OP-1250, is beneath investigation as a therapy for a variety of styles of metastatic breast most cancers, the two as a monotherapy and in mixture with set up therapies.

Final thirty day period, Olema introduced a scientific update on its OP-1250 reports, exhibiting robust development across the method, which consists of two Stage 1b medical trials.

The to start with of these trials is testing OP-1250 as a monotherapy towards ER+ HER2 cancers. This demo, which is inspecting dose growth in preparing for afterwards phase research, has proven both of those favorable tolerability and ‘encouraging’ anti-tumor action. The 2nd Period 1b demo is a blend analyze with Palbociclib, and the 1st two cohorts have done the dose limiting toxicity analysis. That move has shown compatibility in the combination review.

Olema expects further more information releases later this yr to clearly show supplemental validation for OP-1250, and expects to start a pivotal monotherapy study in 2023.

Going forward, to develop new drug candidates, Olema in early June declared a new agreement to start a collaboration with Aurigene in the growth of novel small molecule inhibitors in the oncology field. The settlement will dedicate Olema to pay out $8 million up entrance in licensing expenses, with extra payments to Aurigene as medical milestones are reached.

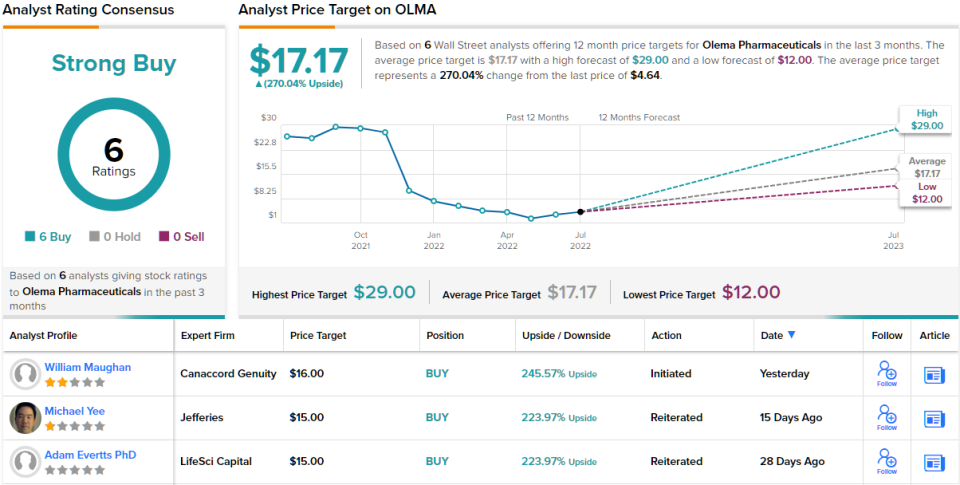

Canaccord analyst William Maughan lays out a crystal clear path for Olema heading to the finish of this yr, composing, “We assume that knowledge updates over the next 12-18 months will aid characterize OP-1250 as a potential best-in-class agent and clarify the clinical advancement pathway, both as a monotherapy and in combination with now authorised brokers… In 2H22 we anticipate mono and original combo details with palbociclib, where we be expecting additive efficacy and will be observing neutropenia fees and continued lack of palbo metabolism alteration from OP-1250. In 2023 Olema expects to initiate a pivotal monotherapy research in ER+/HER2- mBC in 2L+. The design and style will count on forthcoming knowledge, and we glance forward to extra clarity on the drug’s path to marketplace and strategy for medical improvement whilst recognizing that blend remedy likely signifies important upside over and above monotherapy.”

All of this prompted Maughan to charge Olema shares a Buy, together with a $12 rate concentrate on. This concentrate on conveys his self-confidence in OLMA’s capability to climb 250% greater in the future calendar year. (To view Maughan’s keep track of record, click on right here)

All in all, other analysts mirror Maughan’s sentiment. With 100% Road assist, or 6 Invest in rankings to be actual, the consensus is unanimous: OLMA is a Robust Get. Shares are priced at $4.64, and the $17.17 typical concentrate on implies 270% upside from that level. (See OLMA stock forecast on TipRanks)

To discover good thoughts for penny stocks investing at eye-catching valuations, visit TipRanks’ Most effective Stocks to Obtain, a freshly released tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this write-up are exclusively these of the showcased analysts. The information is supposed to be utilized for informational reasons only. It is very essential to do your own analysis prior to generating any financial commitment.